Airline on-time performance—2025 calendar year

Summary – 2025 Calendar Year

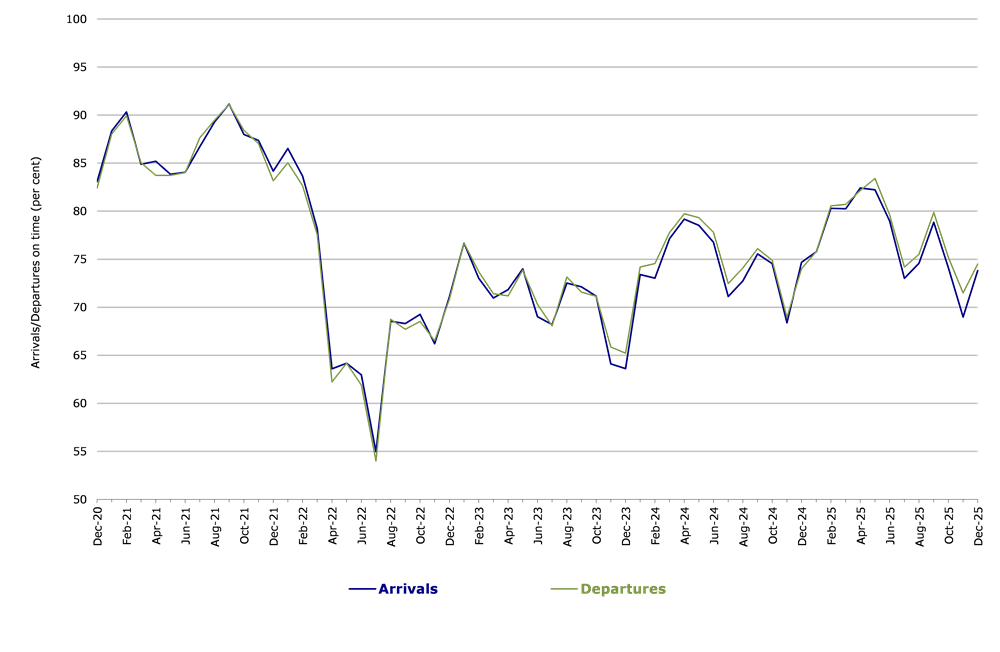

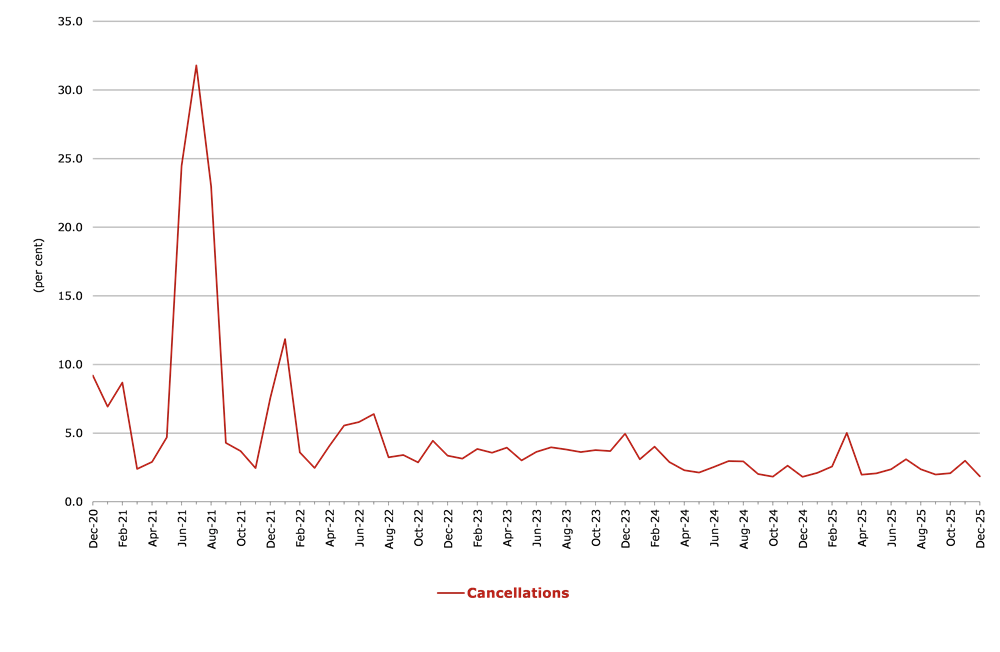

For the year ended December 2025, on time performance (OTP) over all routes operated by participating airlines (Hinterland, Jetstar, Qantas, QantasLink, Rex Airlines, Skytrans Australia (formerly Smartlynx Australia), Virgin Australia and Virgin Australia Regional Airlines) averaged 76.9 per cent for on time arrivals and 77.7 per cent for on time departures. The cancellation rate for the year was 2.5 per cent. The equivalent figures for 2024 were 74.6 per cent for on time arrivals, 75.4 per cent for on time departures and 2.6 per cent for cancellations. Airlines’ on time performance varies across the routes they serve. Individual route data by specific airline for 60 routes which operated for at least part of the 2025 calendar year are shown on pages 9-21.

The 2025 on time arrivals figure was lower than the long-term average (average over the period of OTP reporting starting in November 2003) performance for all routes (80.5 per cent) and the on time departures figure was also lower than the long-term average (81.6 per cent). The rate of cancellations was higher than the long-term average of 2.2 per cent.

On time arrivals

The Qantas network (Qantas and QantasLink combined operations) recorded 77.9 per cent for on time arrivals while the Virgin Australia network (Virgin Australia and Virgin Australia Regional Airlines combined operations) recorded 76.0 per cent. Hinterland achieved the highest on time arrivals at 88.4 per cent, followed by Skytrans Australia at 85.1 per cent, QantasLink at 78.3 per cent, Qantas at 77.2 per cent, Virgin Australia at 76.0 per cent, Jetstar at 75.2 per cent, Rex Airlines at 73.0 per cent and Virgin Australia Regional Airlines at 71.5 per cent.

On time departures

The Qantas network recorded 78.8 per cent for on time departures while the Virgin Australia network recorded 77.0 per cent. Hinterland achieved the highest level of on time departures for 2025 at 92.5 per cent, followed by Skytrans Australia at 86.3 per cent, Qantas at 79.7 per cent, QantasLink at 78.3 per cent, Virgin Australia at 77.2 per cent, Rex Airlines at 76.0 per cent, Jetstar at 73.6 per cent and Virgin Australia Regional Airlines at 67.6 per cent.

Cancellations

Skytrans Australia recorded the highest percentage of cancellations at 8.4 per cent during the year. The second highest cancellation rate was from QantasLink at 3.6 per cent, followed by Qantas at 2.7 per cent, Rex Airlines at 2.5 per cent, Jetstar at 2.2 per cent, Virgin Australia at 1.7 per cent, Virgin Australia Regional Airlines at 1.1 per cent and Hinterland at 0.8 per cent.

Routes

Of the 60 routes which met the criteria for OTP reporting, the Townsville-Cairns route (Jan 2025 only) had the highest percentage of on time arrivals (90.9 per cent) and the highest percentage of on time departures (90.9 per cent). For those routes reporting for the entirety of 2025, Emerald-Brisbane had the highest percentage of on time arrivals (89.8 per cent) and the highest percentage of on time departures (88.4 per cent). The Hamilton Island-Sydney route had the lowest percentage of on time arrivals (60.8 per cent) and the lowest percentage of on time departures (61.6 per cent).

Cancellations were highest on the Canberra-Sydney route at 6.2 per cent, followed by the Sydney-Canberra route at 5.6 per cent, the Port Lincoln-Adelaide and Sydney-Melbourne routes at 4.4 per cent, the Port Macquarie-Sydney and Melbourne-Sydney routes at 4.3 per cent, the Adelaide-Port Lincoln and Gladstone-Brisbane routes at 4.1 per cent, the Sydney-Port Macquarie route at 4.0 per cent and the Devonport-Melbourne route at 3.9 per cent.

Cancellations were lowest on the Melbourne-Ayers Rock at 0.0 per cent, followed by the Sydney-Hamilton Island route at 0.1 per cent, Ayers Rock-Melbourne and Sydney-Cairns routes at 0.3 per cent, and the Perth-Newman and Melbourne-Sunshine Coast routes at 0.4 per cent.

Airports

Of the airports with OTP reporting for 2025, Emerald Airport recorded the highest percentage of on time arrivals (86.2 per cent) and the highest percentage of on time departures (88.4 per cent). Port Macquarie Airport recorded the lowest percentage of on time arrivals (70.0 per cent) and Broome Airport recorded the lowest percentage of on time departures (64.8 per cent). These figures only refer to reported routes and do not cover all flights at these airports.

Table 1: Total industry on-time performance for 2025

| Reporting Airlines | Sectors Scheduled | Arrivals On Time % | Departures On Time % | Cancellations % |

|---|---|---|---|---|

| Hinterland | 18,415 | 88.4 | 92.5 | 0.8 |

| Jetstar | 96,686 | 75.2 | 73.6 | 2.2 |

| Qantas - all QF designated services | 231,962 | 77.9 | 78.8 | 3.2 |

| Rex Airlines | 52,716 | 73.0 | 76.0 | 2.5 |

| Skytrans Australia (formerly SmartLynx Australia) | 6,191 | 85.1 | 86.3 | 8.4 |

| Virgin Australia - all VA designated services | 145,379 | 76.0 | 77.0 | 1.7 |

| All Airlines | 551,349 | 76.9 | 77.7 | 2.5 |

| Individual operating entities | ||||

| Qantas | 88,886 | 77.2 | 79.7 | 2.7 |

| QantasLink | 143,076 | 78.3 | 78.3 | 3.6 |

| Virgin Australia | 143,031 | 76.0 | 77.2 | 1.7 |

| Virgin Australia Regional Airlines | 2,348 | 71.5 | 67.6 | 1.1 |

Figure 1. Total Industry Arrivals and Departures On Time by month from December 2020

Figure 2. Total Industry Cancellations by month from December 2020

Infrastructure and the Economy

Chapter 1

This chapter provides data on the Australian economy including the value added by Australian infrastructure industries in addition to:

- employment in the transport, energy, communication and water industries

- average weekly earnings for road, rail, water and air and space industries

- price indices

- population

- 9.2 per cent of Australia’s GDP was accounted for by Australia’s major infrastructure industries in 2022-23.

- 1 million people were employed in Australia’s major infrastructure industries in August 2023.

- $1,441 is the average weekly earnings for the road transport industry in 2021.

- 84 per cent of people employed by the road transport industry identify as male.

The gross value added of major infrastructure industries as a percentage of GDP has remained relatively stable since 1974-75, generally ranging between 9-10% of GDP, with the transport postal and warehousing industry specifically ranging between 4-5% over the same timeframe. In terms of employment, although employment in the transport, postal and warehousing industry have grown in overall terms, as a percentage of total Australian employment, it has stayed at around 5% for the last 30 years.

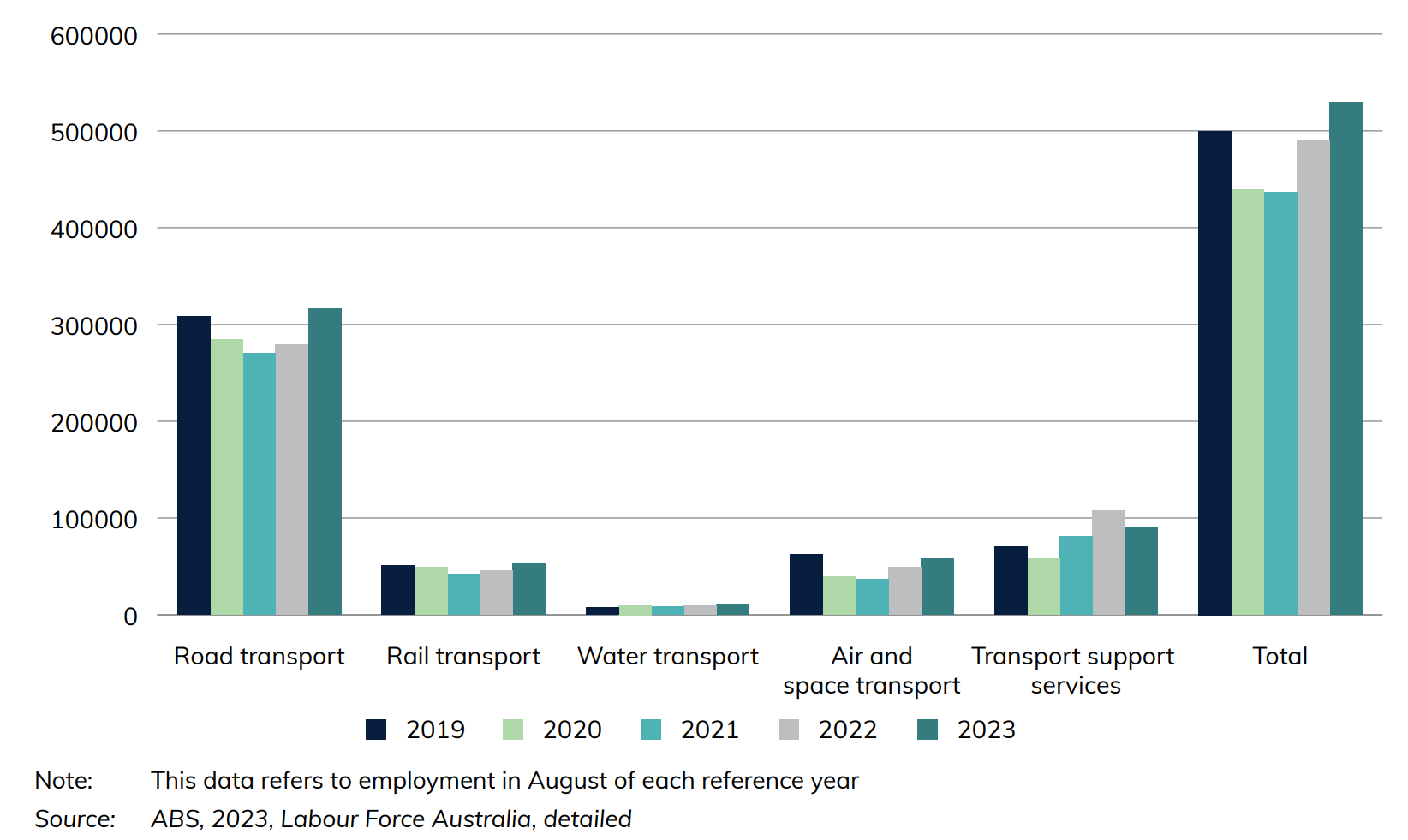

Figure 1 Australian employment numbers in selected major infrastructure industries

Figure 1 shows employment statistics for various transport industries as at August of each year. Although in 2021 COVID-19 had reduced Australian employment numbers in road, rail, and air and space transport industries, this year has shown signs of recovery, closing in on 2019 pre-pandemic levels.

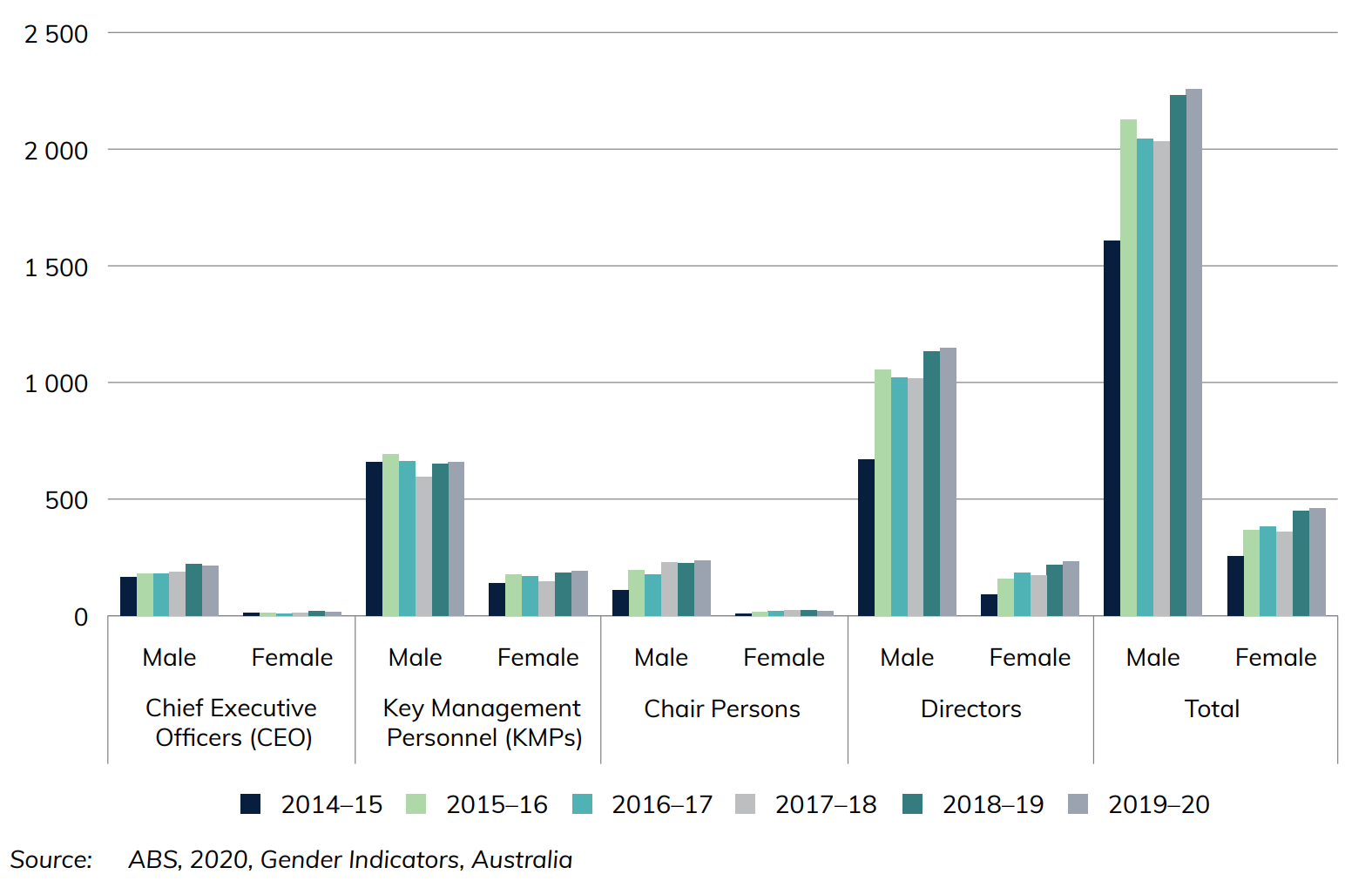

Figure 2 Leadership positions held in transport industries, by gender

Figure 2 provides an insight into gender statistics by comparing the number of leadership positions held by men and women within the transport industry. In 2019, leadership positions in the transport industry were predominantly occupied by males, with 2258 males in Chief Executive Officer, Key Management Personnel, Chair Person and Director roles compared to 460 females.

Download data

Also see

Road-related Revenue and Expenditure

Chapter 3

This chapter provides information on the Government’s total expenditures and sources of revenue for road-related activities for the Commonwealth, state and local Government (noting only expenditure is shown at the local level). A variety of sources are used for this data, including data from the Australian Tax Office, the Australian Bureau of Statistics, the Department of Infrastructure, Transport, Regional Development, Communications and the Arts, BITRE estimates and State and Territory Governments.

- Road related expenditure by all government slightly increased from $33 billion in 2020-21 to $36 billion in 2021-22 (latest available year).

- $28 billion in road-related revenue was collected by all government (excluding road-related revenue from the Goods and Services Tax, Fringe Benefits Tax and the Luxury Car Tax).

Figure 1 Road-related expenditure, by level of government (constant 2021-22 prices, adjusted by CPI)

Government’s road-related expenditure over time can be seen in Figure 1. The State/Territory Government expenditure is at an all-time high in 2021-22 at 23 billion dollars. The Commonwealth’s expenditure fell to 7.7 billion dollars in 2021-22 from a record high of 9.5 billion dollars the previous year. Local government expenditure has remained relatively stable over time, with an average of 5.8 billion dollars over the past 24 years.

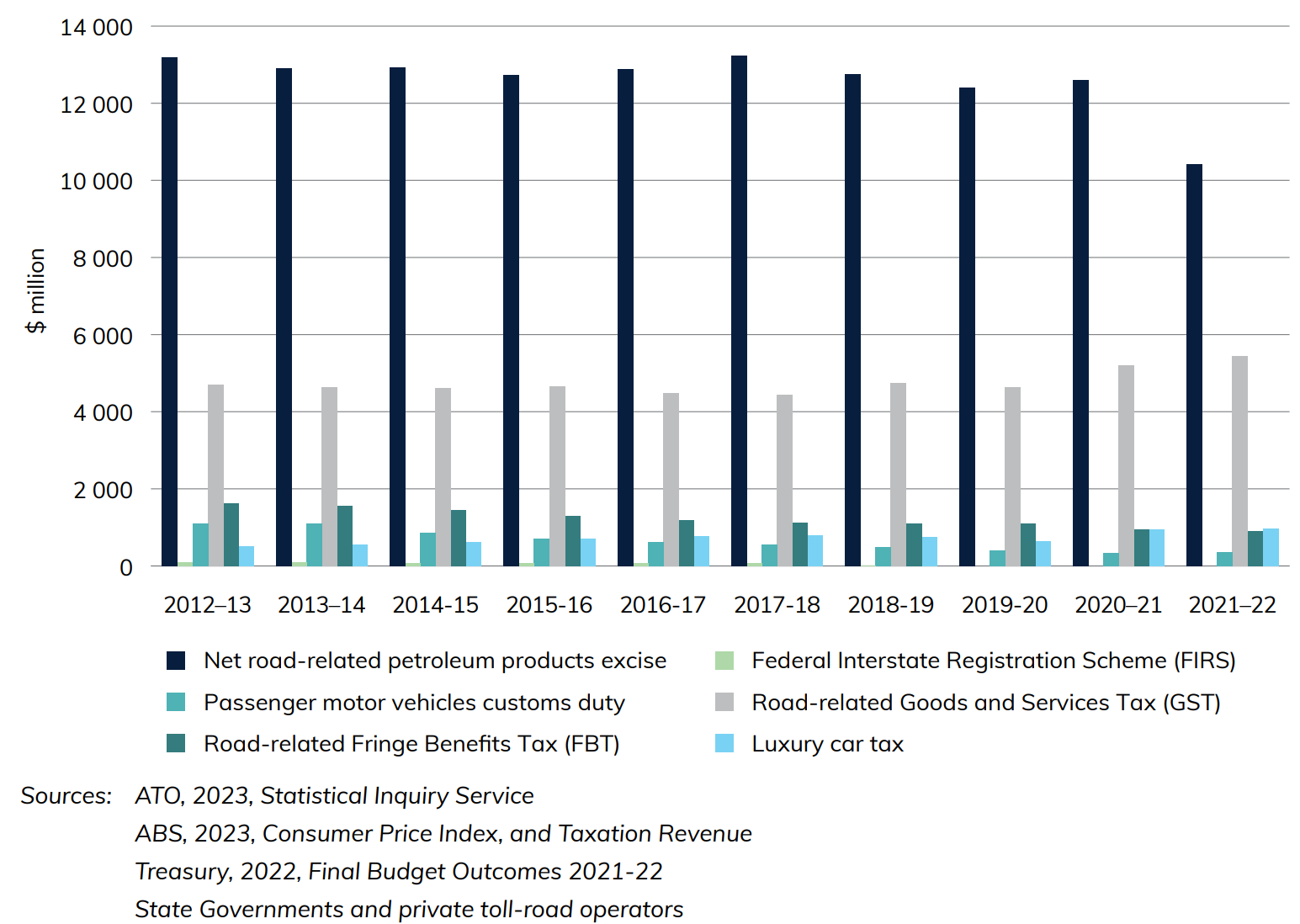

Figure 2 Australian Government Road-Related Revenues

Figure 2 shows road-related revenues for the Australian Government, while Figure 3 shows revenues for the States and Territories (excluding tolls). Figure 2 highlights how the Commonwealth’s main source of road-related revenue is from the net road-related petroleum excise with an average of 12.6 billion dollars over 10 years.

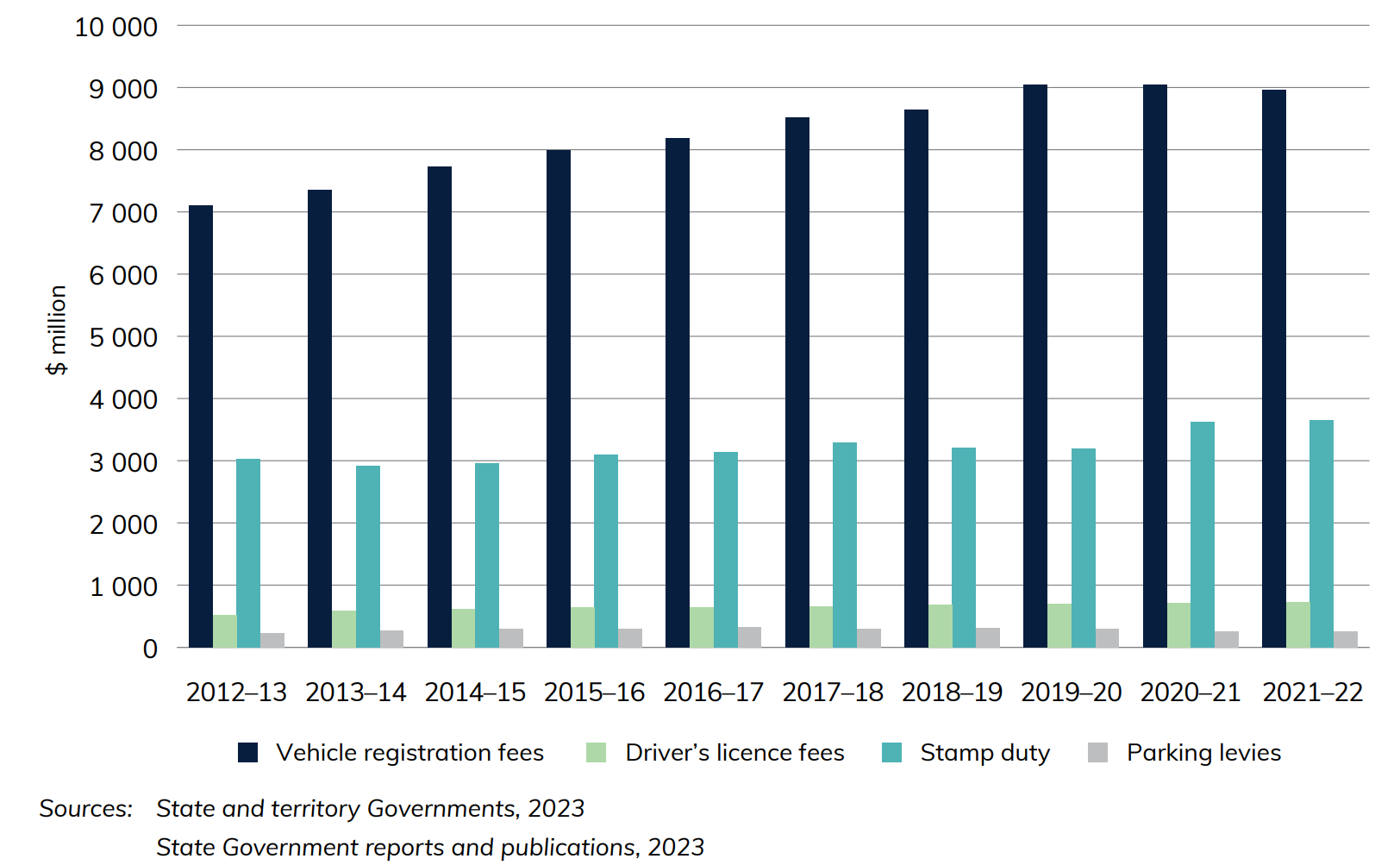

Figure 3 State and Territory Government Road-Related Revenues (excluding tolls)

Figure 3 illustrates that the majority of revenue for the states/territories is vehicle registration fees with an average of 8.3 billion dollars per year over 10 years and a maximum of 9.1 billion dollars in 2020-21.

Download data

Also see

Infrastructure Construction

Chapter 2

This chapter provides information on Australian measures of infrastructure engineering construction. These are classified as: transport (roads, rail, ports, etc), energy (electricity and gas transmission networks, etc), telecommunications networks, and water supply and distribution networks. Data is sourced from the Australian Bureau of Statistics Engineering Construction Activity, Australia publication with some adjustments, as well as the Electric Vehicle Council.

- 559 DC fast and Ultrafast public charging sites were available for Australians to charge their electric vehicles in 2023.

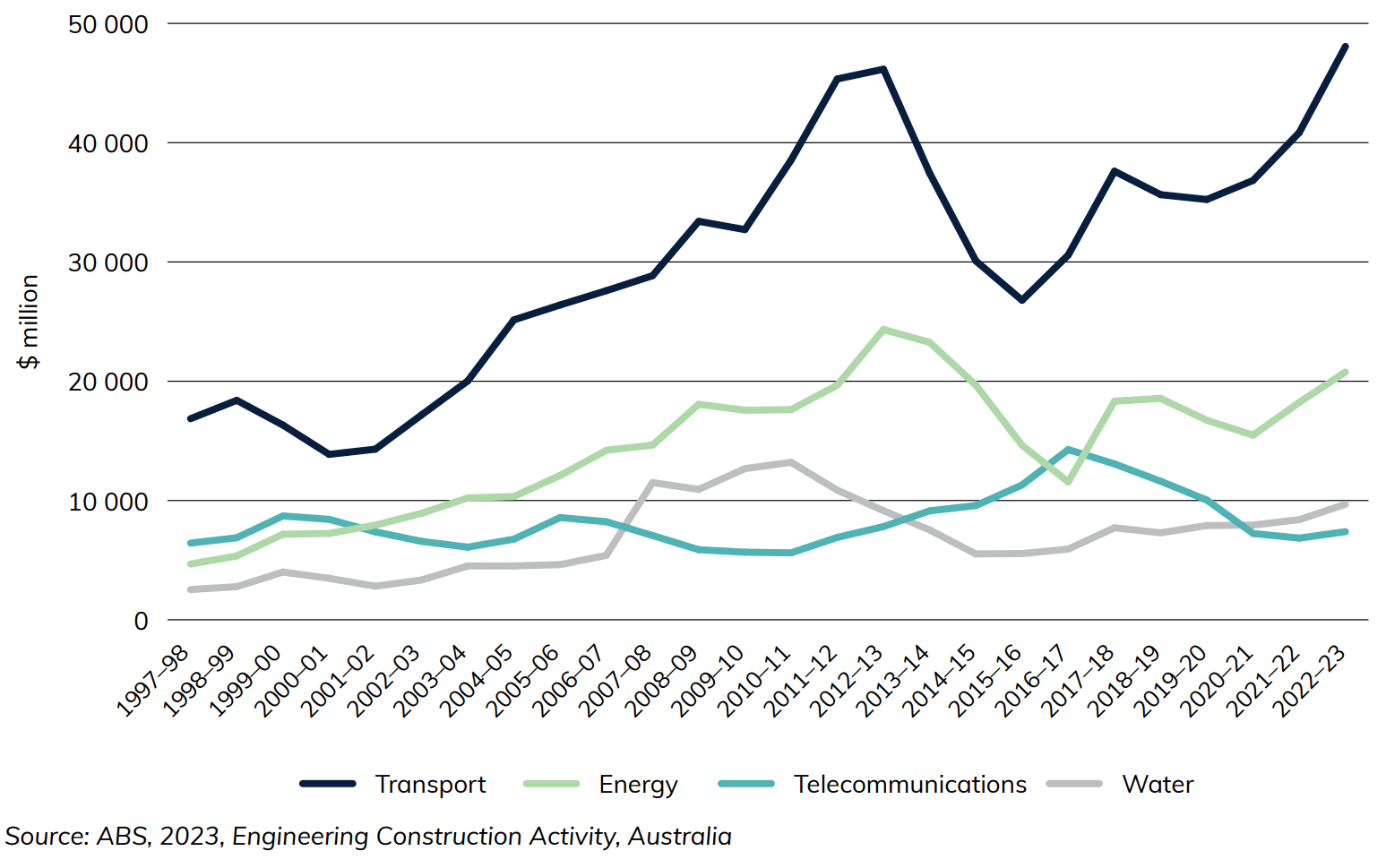

- Transport infrastructure engineering construction work done recorded a new all-time high of $48 billion (adjusted by chain volume index) in 2022-23. This accounted for 56 per cent of all infrastructure engineering construction work done in Australia.

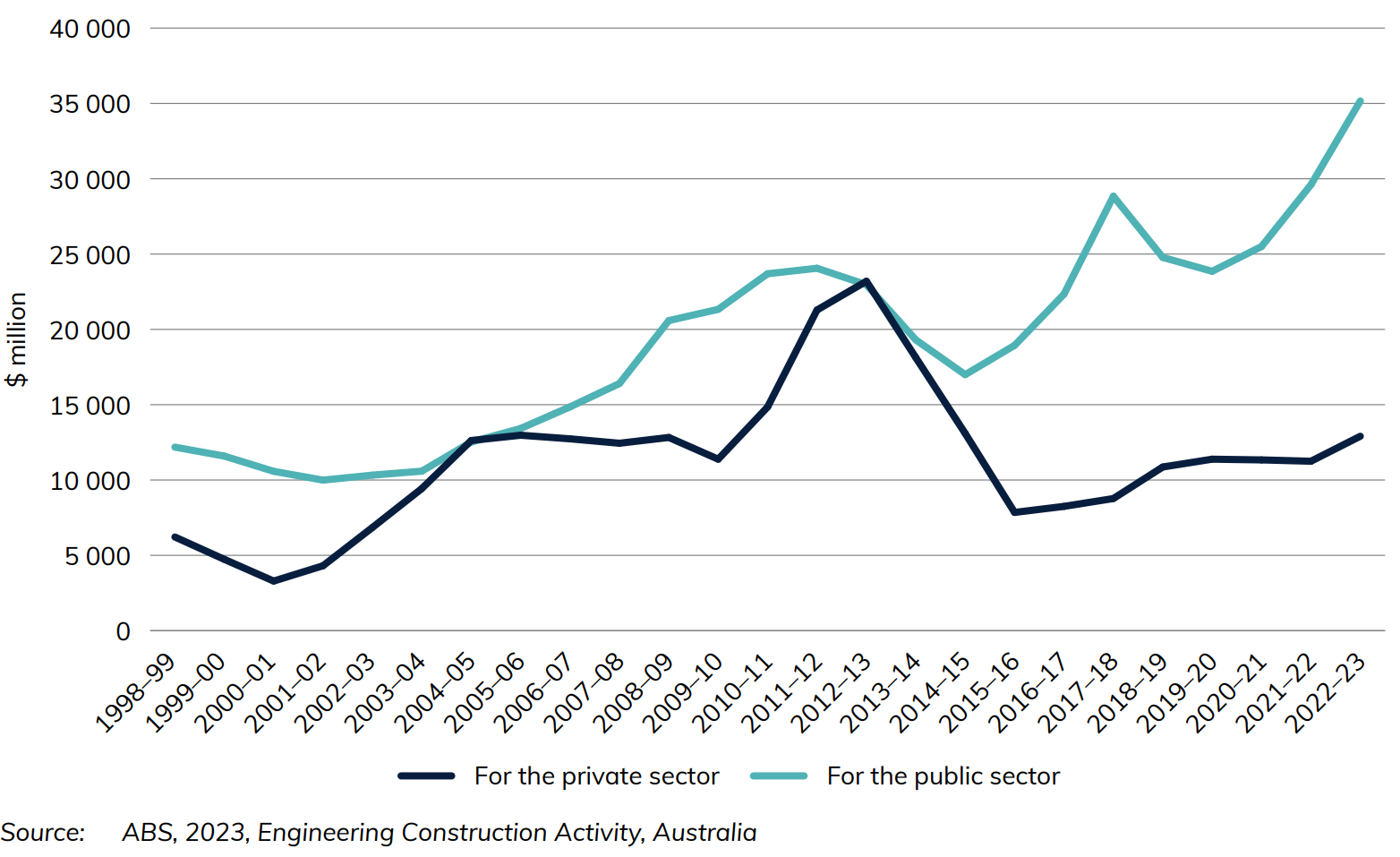

Figure 1 Infrastructure construction activity adjusted by chain volume index

Figure 1 and Figure 2 show the change in infrastructure investment activity in Australia over time. Transport, water and energy investment increased relatively consistently until roughly 2012-13, when they each experienced a notable fall. They have recovered in recent years, however, with the Transport sector reaching its new highest point of roughly $48 billion in 2022-23 (Figure 1).

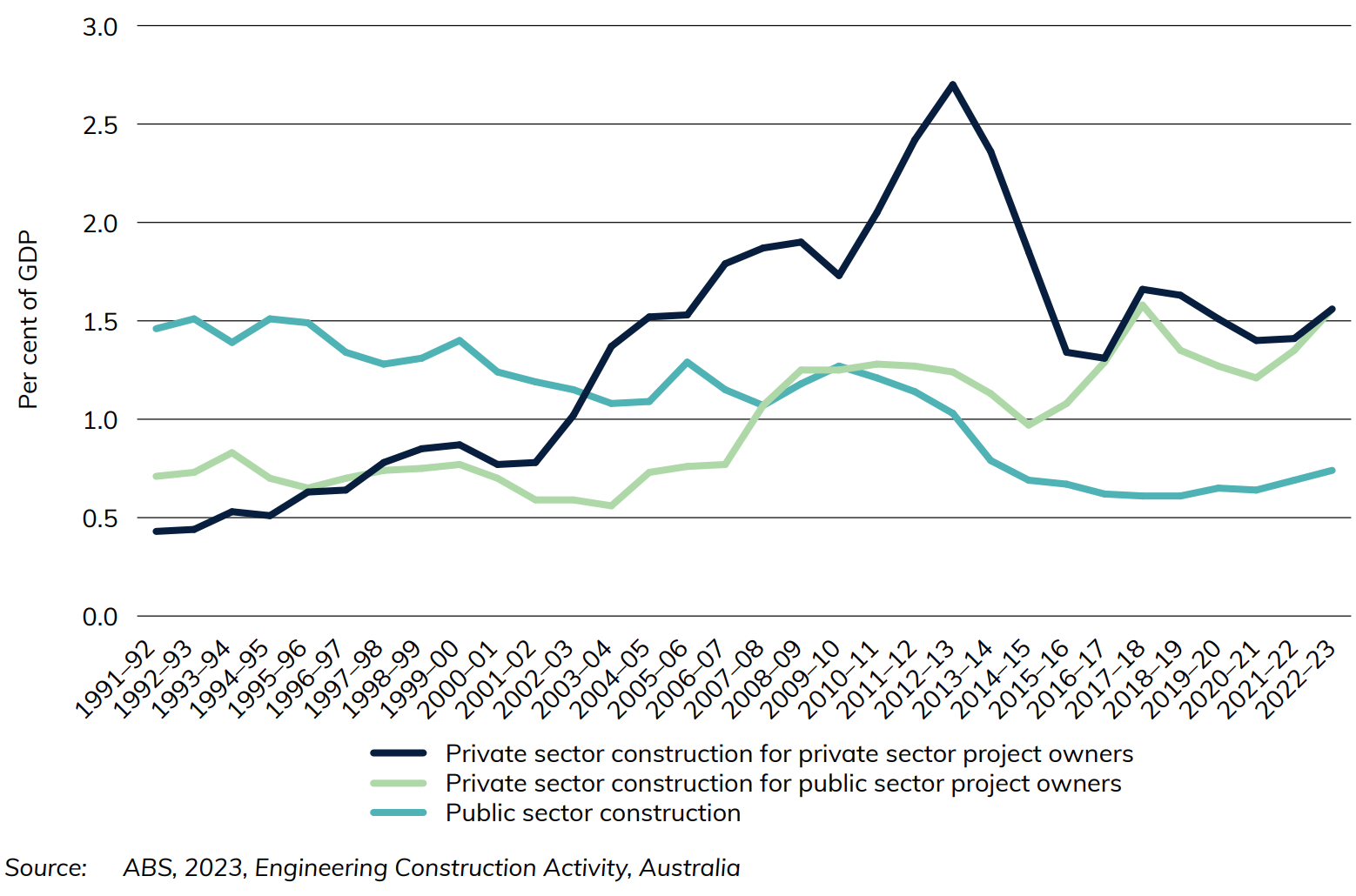

Figure 2 Infrastructure construction activity, by sector, adjusted by chain volume index

Figure 2 illustrates the private and public sector changes in Australian infrastructure expenditure as a percentage of national GDP. Both public and private sector construction activities are derived from the activity by major forms of infrastructure: transport, energy, telecommunications and water supply.

Figure 3 Value of transport infrastructure spending, adjusted by chain volume index

Download data

Also see

Australian Infrastructure and Transport Statistics Yearbook 2023 and Freight chapter

Chapter 4

Download data

Australian

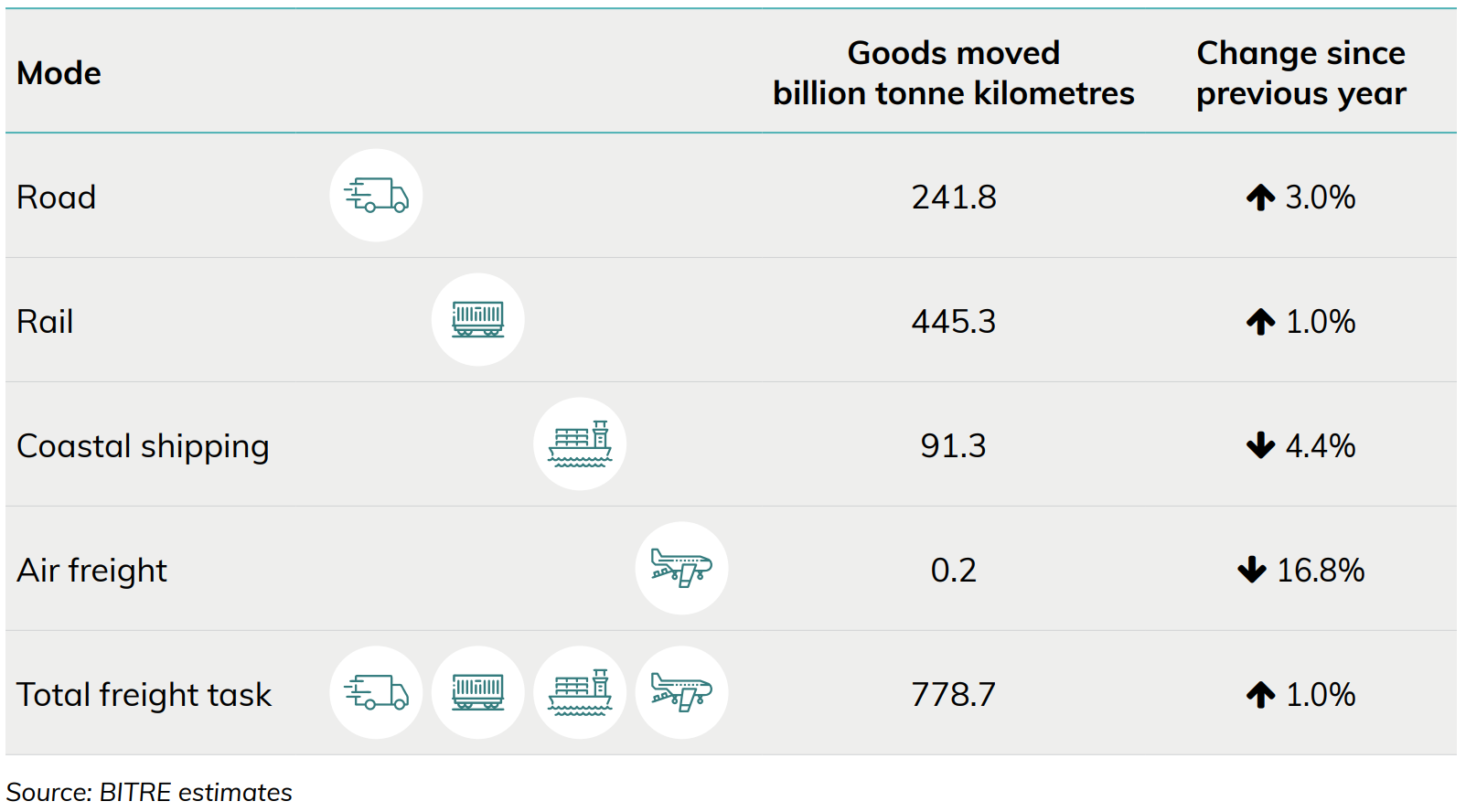

This chapter focuses on Freight and explores the amount of goods moved in the Australian economy. The data from this chapter is sourced from BITRE’s Trainline and Australian Sea Freight publications, along with other unpublished estimates.

- Melbourne had the most metropolitan road fright estimated at 17.1 billion tonne‑kilometres in 2022‑23.

- NSW’s estimated road freight for 2022-23 was the highest on record at 84 billion tonne‑kilometres.

Figure 1 Australia’s Domestic freight, 2022-23

Freight transport activity (Figure 1) is measured in terms of tonne kilometres (the number of tonnes moved by a vehicle multiplied by the distance the load travelled in kilometres).

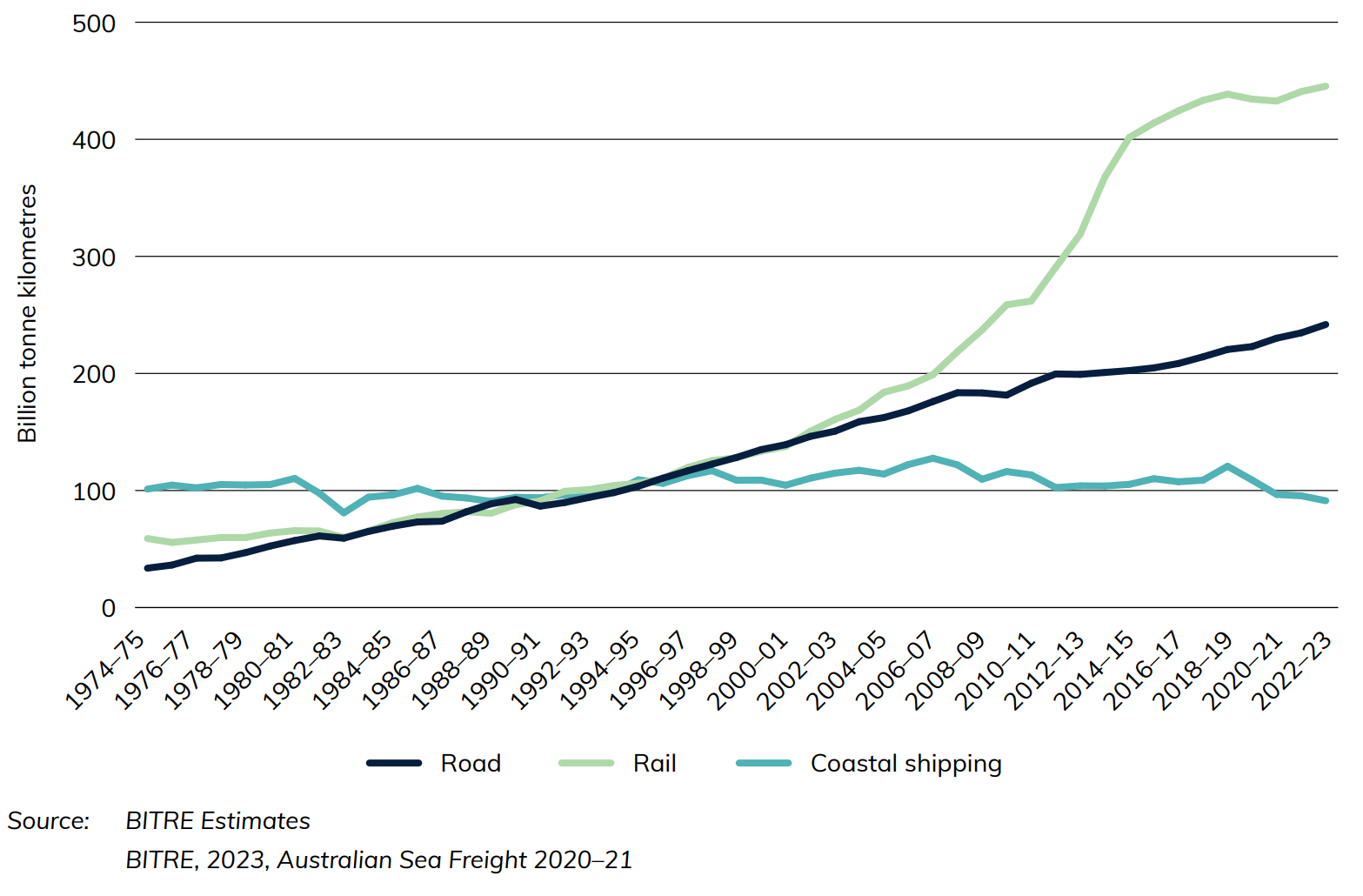

Figure 2 Australian domestic freight task, by mode of transport

The Australian domestic freight task (Figure 2) has experienced strong growth over the last 40 years, with road and rail freight now dominating domestic freight activity. During the COVID-19 pandemic, the total bulk and non-bulk freight task fell slightly, from its height of 780.0 billion tkm in 2018-19 to 759.7 billion tkm in 2020-21. It has grown over the last two years, however, reaching its second-highest point in 2022-23 of 778.7 billion tkm.

Also see

Chapter 5

This chapter provides information on passenger transport activity, including nationally, by city pair, by capital city and by method of travel to work. The data in this chapter comes from a variety of sources, being from BITRE’s estimates, the ABS’ Census Basic Community Profiles Series and from Tourism Research Australia.

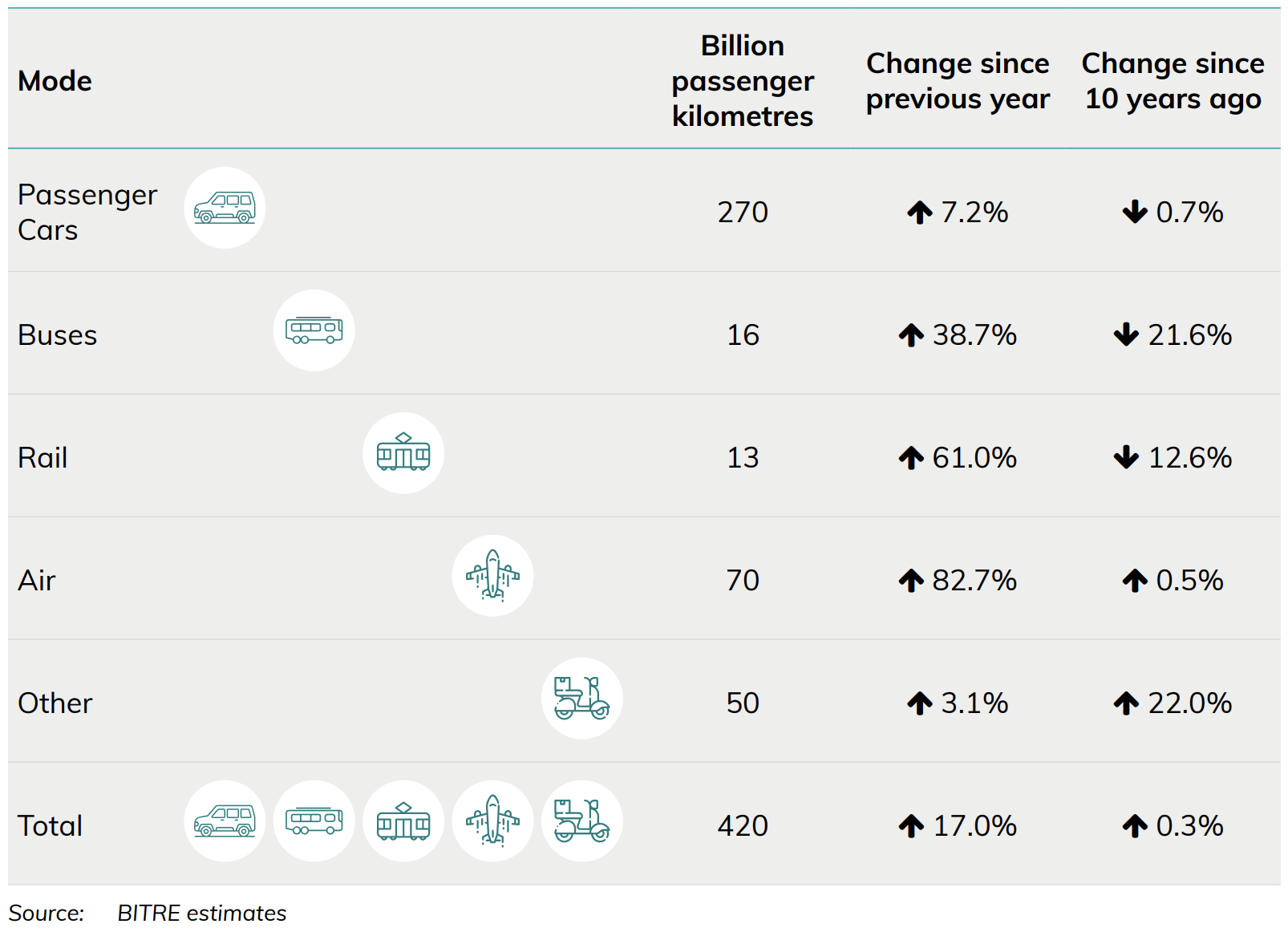

- 158 billion passenger kilometres were travelled by car on capital city roads in 2022-23.

- 10.5 billion passenger kilometres were travelled on heavy rail networks in 2022-23.

- 164 billion passenger kilometres were travelled by car on capital city roads in 2018-19, prior to any COVID impacts.

- 14.8 billion passenger kilometres were travelled on heavy rail in 2018-19, prior to any COVID impacts.

Figure 1 Australia’s National Passenger travel, 2022-23

Passenger transport activity (Figure 1) is measured by passenger kilometres (the number of kilometres travelled by passenger vehicles multiplied by the number of occupants in the vehicle).

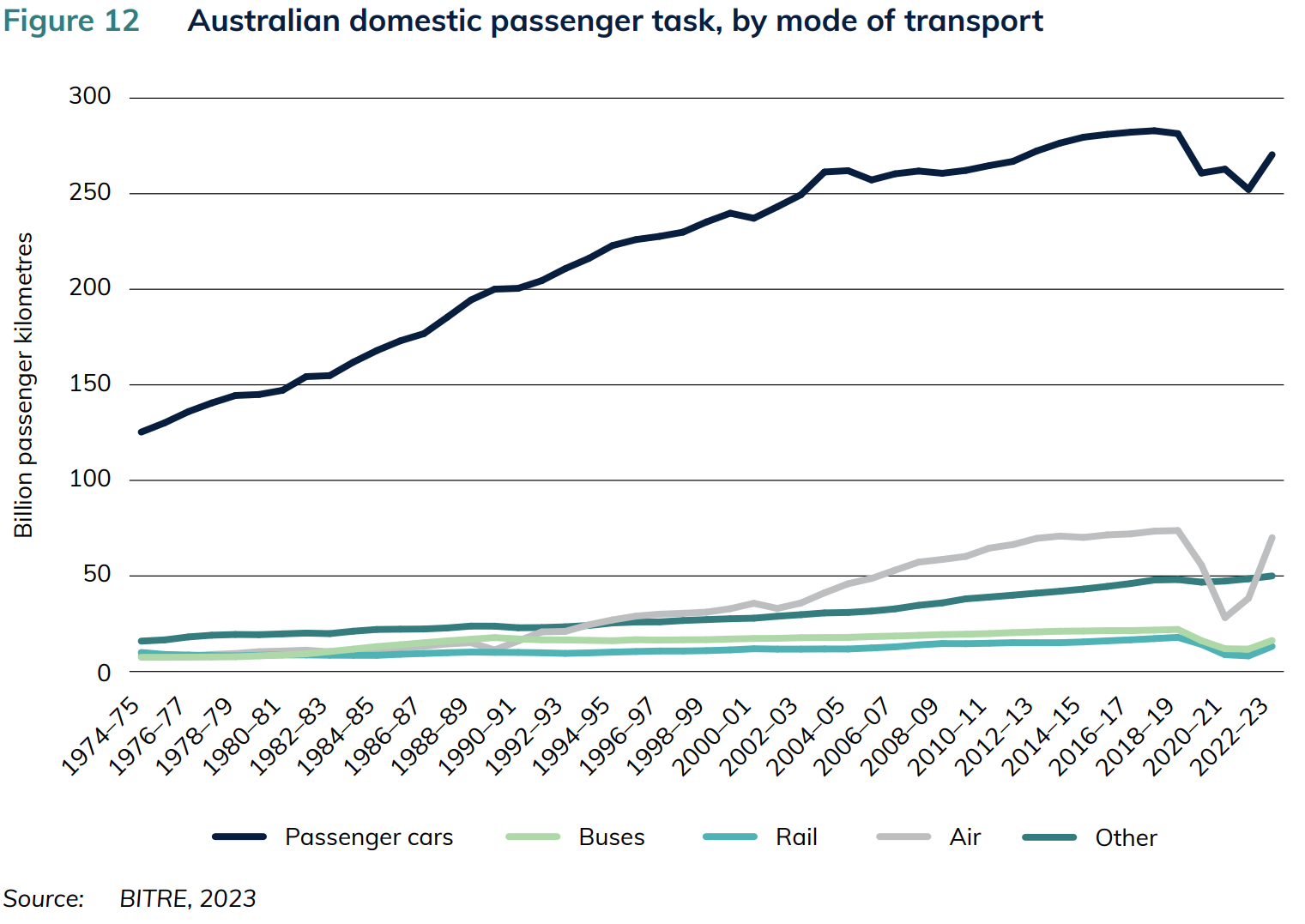

Figure 2 Australian domestic passenger task, by mode of transport

The Australian domestic passenger task is dominated by road transport, mainly passenger cars (Figure 2). Passenger travel on other modes has generally been increasing, albeit with a dip over the pandemic period. Air travel expectedly fell most significantly, however in 2022-23 it had recovered to near its pre-pandemic level.

Download data

Also see

Chapter 6

This chapter provides the following information on Australian roads: road distances, road length in kilometres, licence registration transactions over different vehicle types, electric vehicles attributes and registration transactions.

A variety of sources are used for this data, including data from the Australian Bureau of Statistics, the Department of Infrastructure, Transport, Regional Development, Communications and the Arts, Federal Chamber of Automotive Industries (FCAI), VFACTS, BITRE estimates and State and Territory Governments.

- Australia’s total estimated paved road length was 427,000 kilometres in 2022.

- An estimated 254 billion vehicle kilometres were travelled on Australia's roads in 2022-23.

- In 2022-23, Sports Utility Vehicles (SUVs) comprised 55% of new motor vehicle sales (excluding motor cycles) compared with only 28% 10 years earlier.

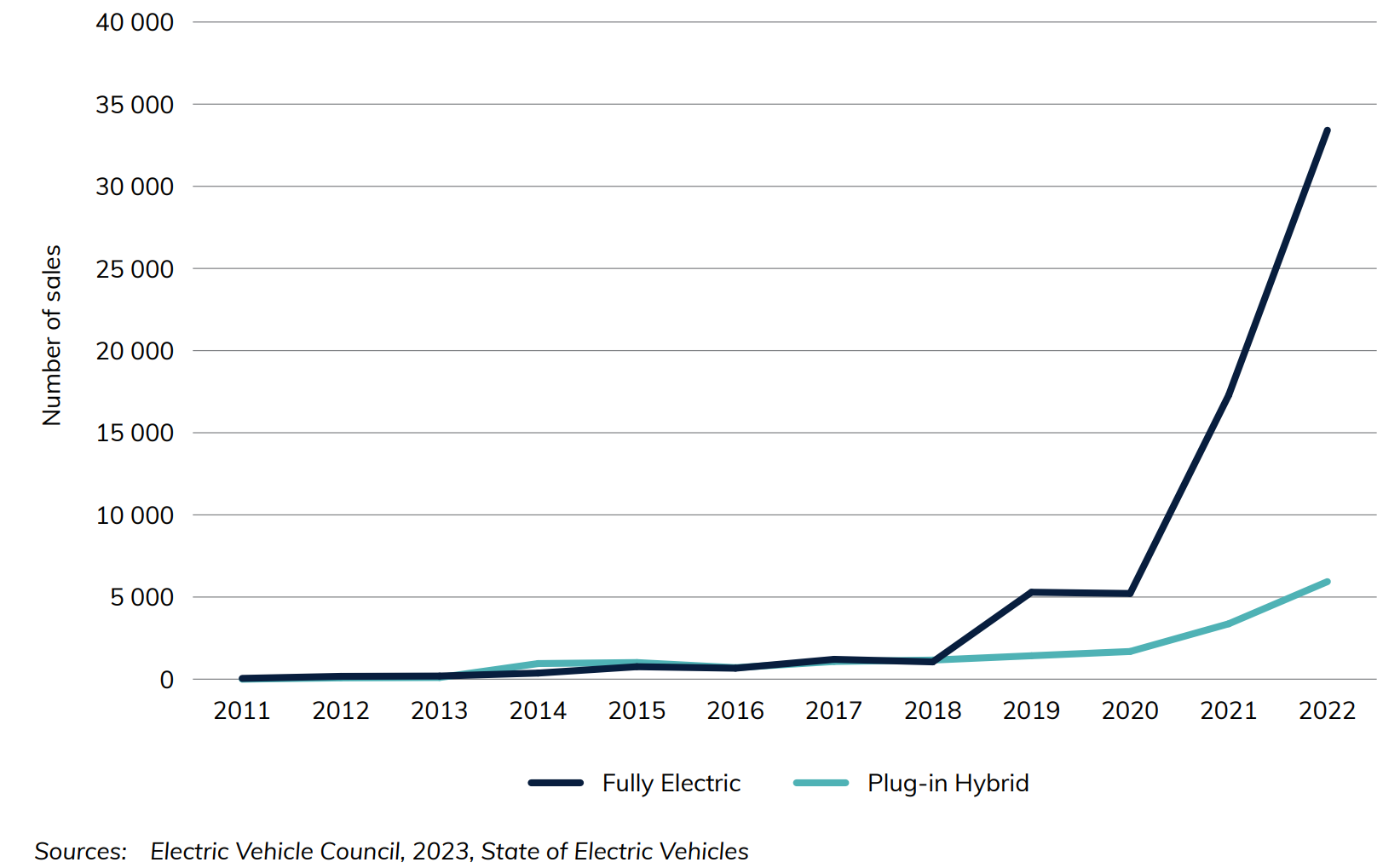

- In 2022, there were 33 000 electric vehicle sales in Australia, up from 17 000 the previous year.

Figure 1 Map of national road network

Figure 1 shows Australia’s national road network. The lines and dots shown here are the roads and town points that were open for traffic at December 2021.

Figure 2 Sales of electric vehicles

Figure 2 shows the sale of registered battery electric vehicles and Plug-in Hybrids over time. Fully battery electric vehicles sales increased by 93 per cent between 2021 and 2022.

Download data

Also see

Australian Infrastructure and Transport Statistics Yearbook 2023 and Rail chapter

Chapter 7

Download data

Chapter 7 provides information on rail lengths, rail interstate non-bulk freight, public transit patronage on rail and rail related expenditure. The data is sourced mainly from BITRE and the Australian Bureau of Statistics.

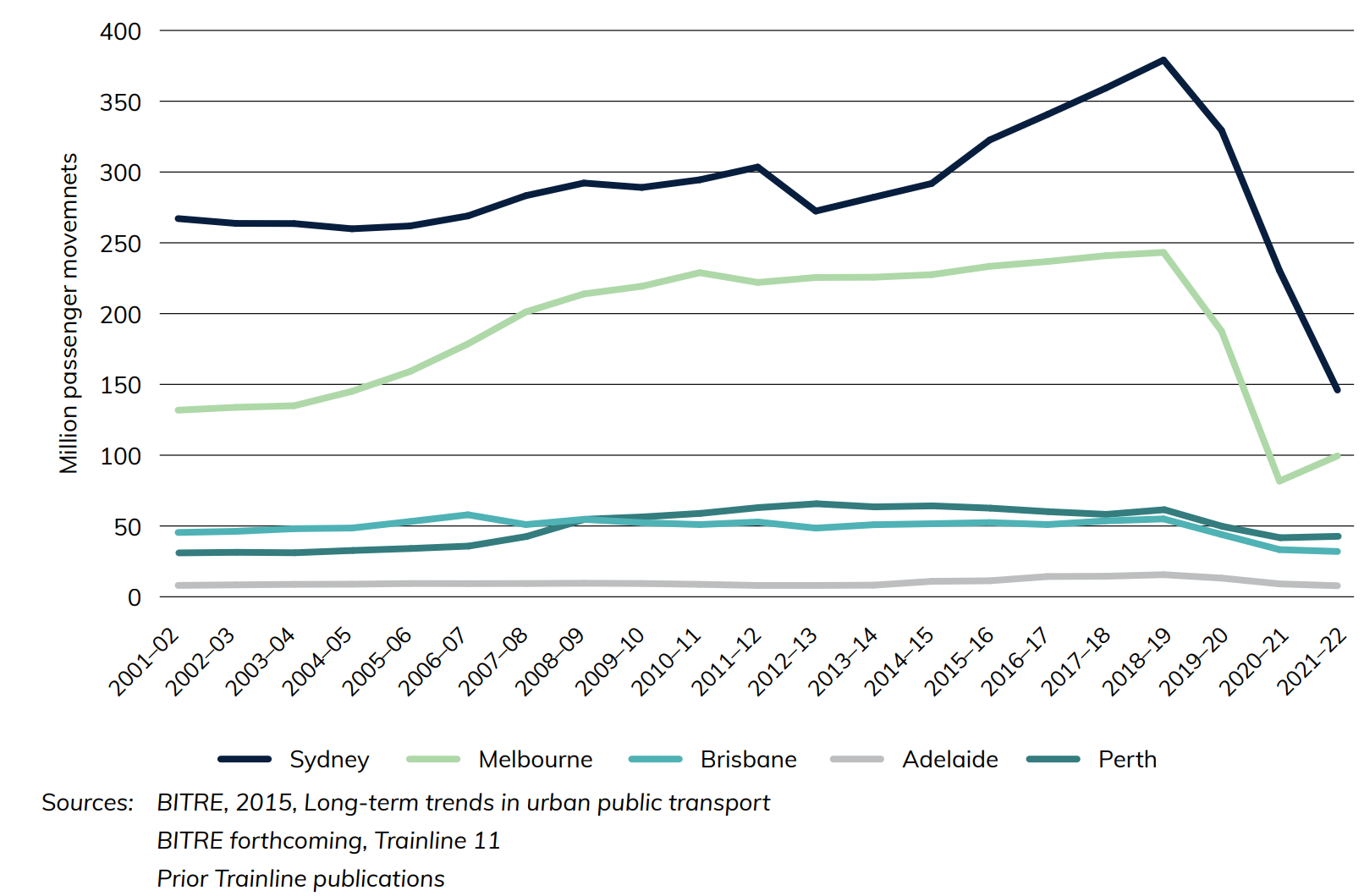

- People in Melbourne use light rail more than any other city with 205 million passengers in 2018-19 (before COVID impacts).

- People in Sydney use heavy rail more than any other city with 379 million passengers in 2018-19 (before COVID impacts).

- 18.2 billion dollars was spent by all government on rail related projects in 2021-22.

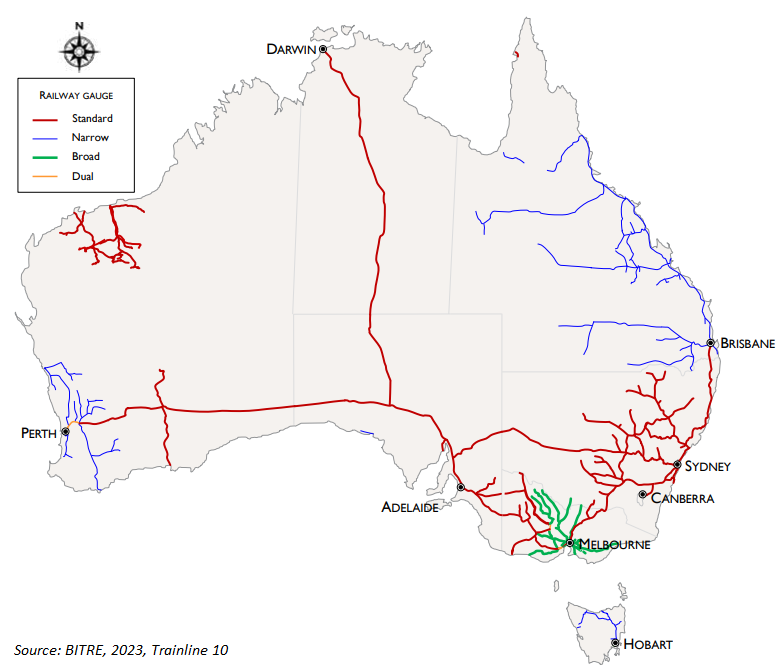

Figure 1 Australia’s railways, by gauge

The lines shown in Figure 1 are the railways that were open for traffic at October 2022. The only change since 2021 was the opening of the Forrestfield-Airport Link (Metronet) line in Perth.

Figure 2 Public transit patronage on heavy rail, Australian capital cities

Figure 2 shows rail public transport patronage by million passenger movements. Passenger movements were trending upwards in Sydney, Melbourne, Perth and Adelaide before starting to fall sharply in 2019-20 due to the COVID-19 pandemic. While Melbourne’s passenger numbers began to recover in 2021-22, Sydney’s continued to decline rapidly, recording a larger proportional fall than in each of the two preceding years. This refers to all trips on suburban rail networks and is based on reporting from train operators.

Chapter 8

This chapter provides data on airline activity, aircraft numbers, on time performance and airfare price indexes. Information is provided for both international and domestic airlines, as well as a breakdown of airport traffic by state.

- 595 118 Australian domestic flights occurred in 2022-23. As with internal activity, the full recovery of the aviation industry to pre COVID levels has not yet occurred. At the height of the pandemic, domestic flights fell to 324 616, fewer than flight numbers in 1977-78.

- 11 020 Piston aircraft were registered in 31 December 2022 which is 1 011 more than the year before. This is the greatest increase recorded. The number of helicopters registered fell from 2 467 to 2 351 over the same period.

- Sydney had the most aircraft movements with 282 251 in 2022-23.

- International flights from Australia are steadily recovering from the impacts of COVID. In 2022‑23 there were 150 684 flights, up from only 45 172 two years earlier.

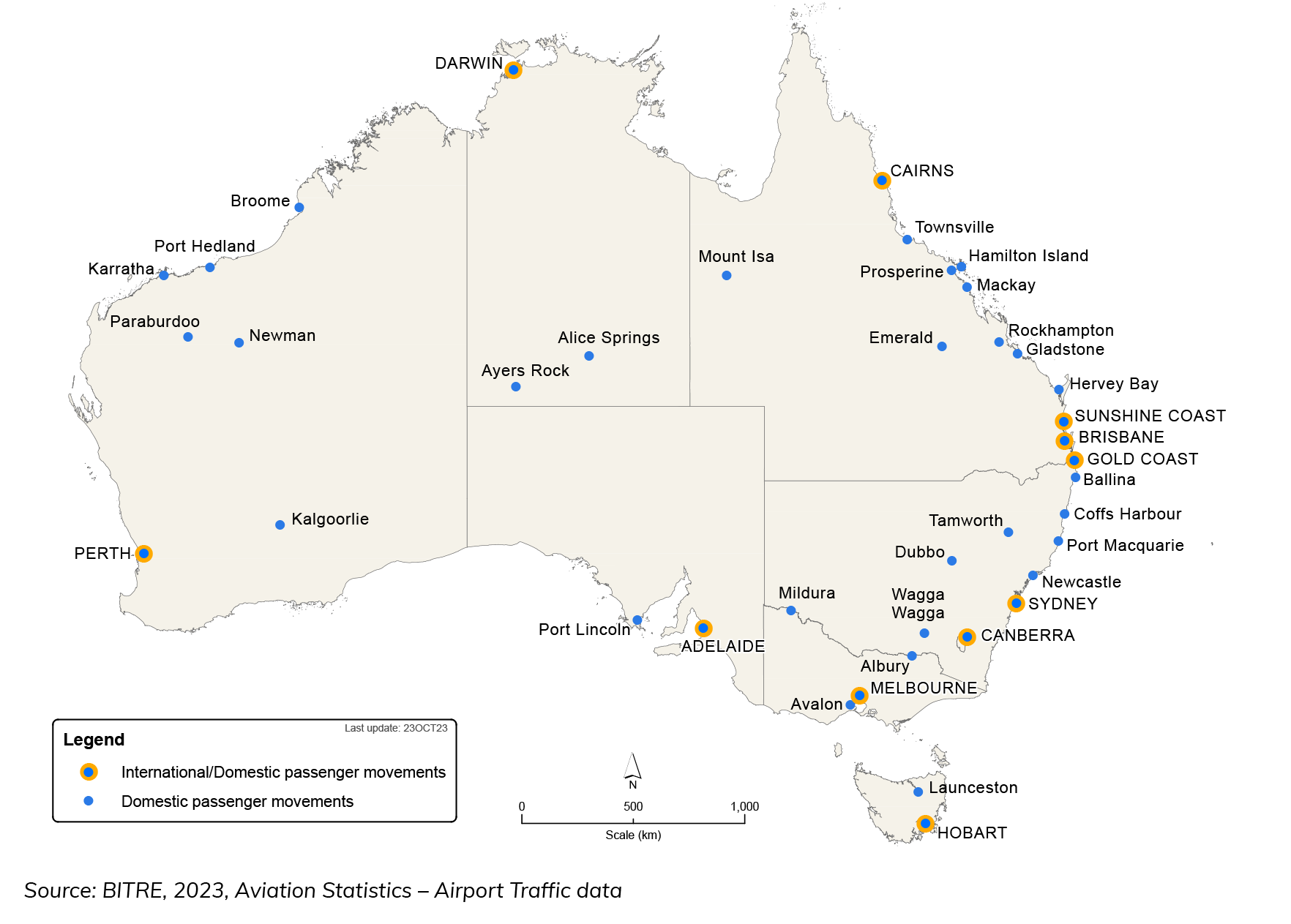

Figure 1 Australia’ top 40 airports in 2022-23, passengers

Since 2019-20, Sydney, Melbourne and Brisbane have remained the airports which experienced the most activity, with some regional airports outside of the top 30 entering and exiting the list.

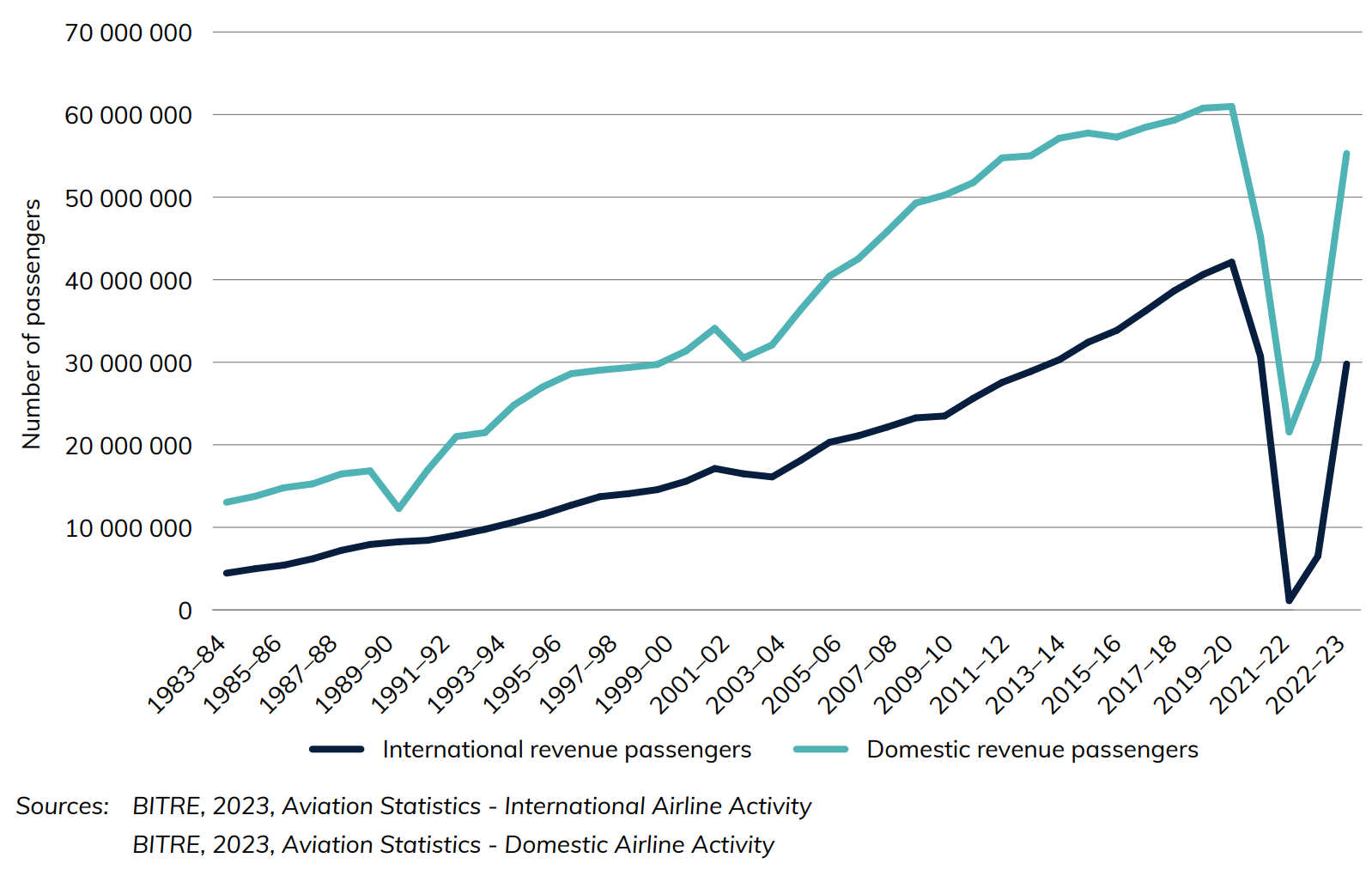

Figure 2 International and domestic airline revenue passengers

Since 1977-78, the number of fare-paying passengers uplifted and discharged in Australia was steadily increasing both domestically and internationally, before a sharp drop beginning in 2019-20. 2021-22 shows some evidence of an improvement as border restrictions due to the COVID-19 pandemic ease.

Download data

Also see

Australian Infrastructure and Transport Statistics Yearbook 2023 and Shipping chapter

Chapter 9

Download data

This chapter provides information on Australian ships, cargo, ports and fleet including mileage, tonnage and number of vessels. The data is sourced from BITRE’s Australian Sea Freight publication, BITRE’s Waterline publication and BITRE estimates based on Lloyds List Intelligence Data.

- There were 55 Australian registered vessels in the Australian trading fleet, including small vessels, and 73 overseas registered vessels in 2021-22.

- Queensland had the largest discharged volume with 40 million tonnes in 2020-21. Following Queensland, was New South Wales and Victoria with 33 million tonnes discharged each.

- Western Australian ports loaded 1 004 million tonnes of maritime cargo in 2020-21, the largest volume in Australia. Next, Queensland and New South Wales loaded 289 million tonnes and 176 million tonnes respectively. Together the ports in these three states loaded 94 per cent of Australia's maritime cargo by volume in 2020‑21.

- 8.6 million TEUs (twenty-foot equivalent units) were exchanged at container terminals in Brisbane, Sydney, Melbourne, Fremantle and Adelaide in 2022-23.

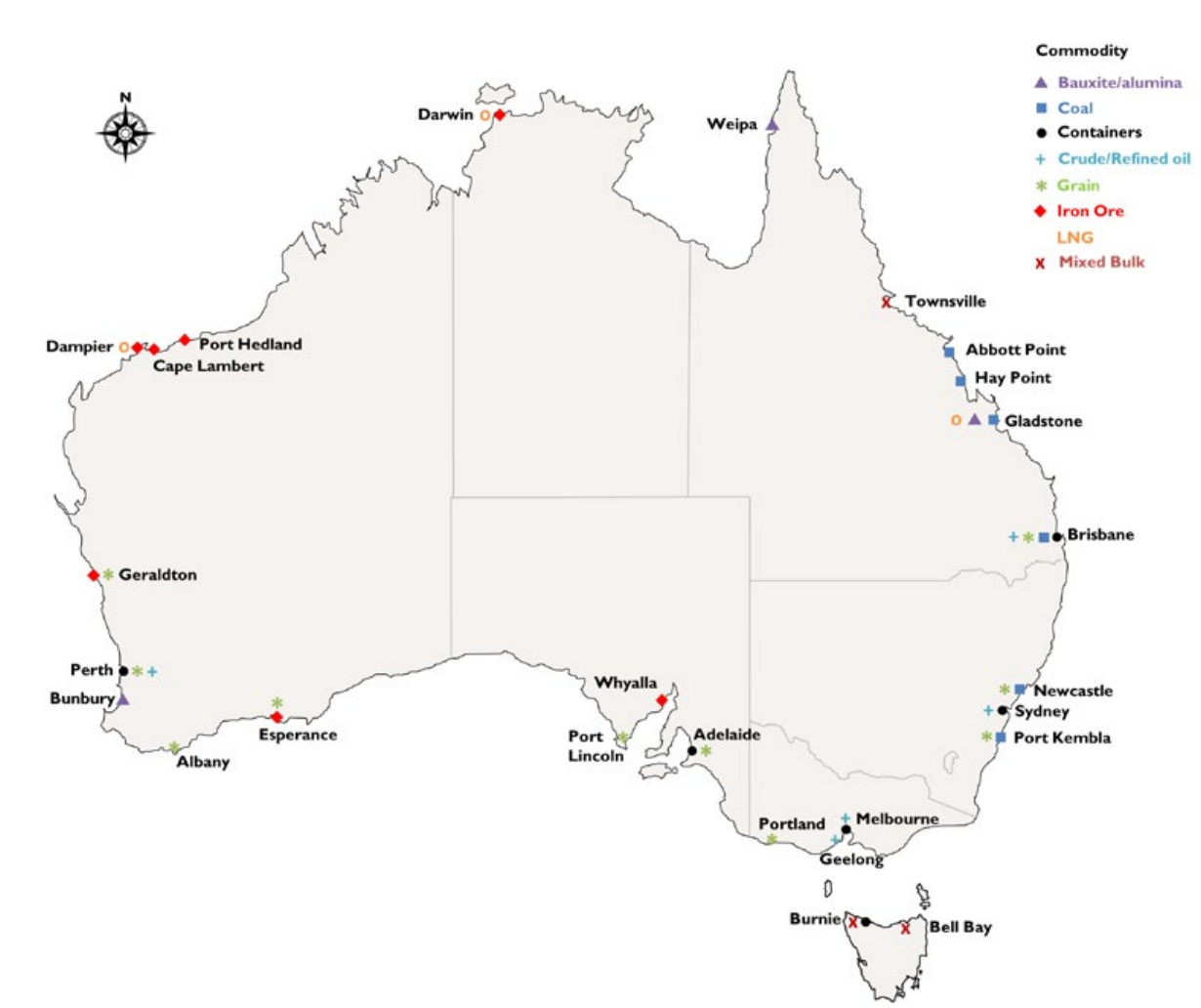

Figure 1 Principal Australian ports, by commodity

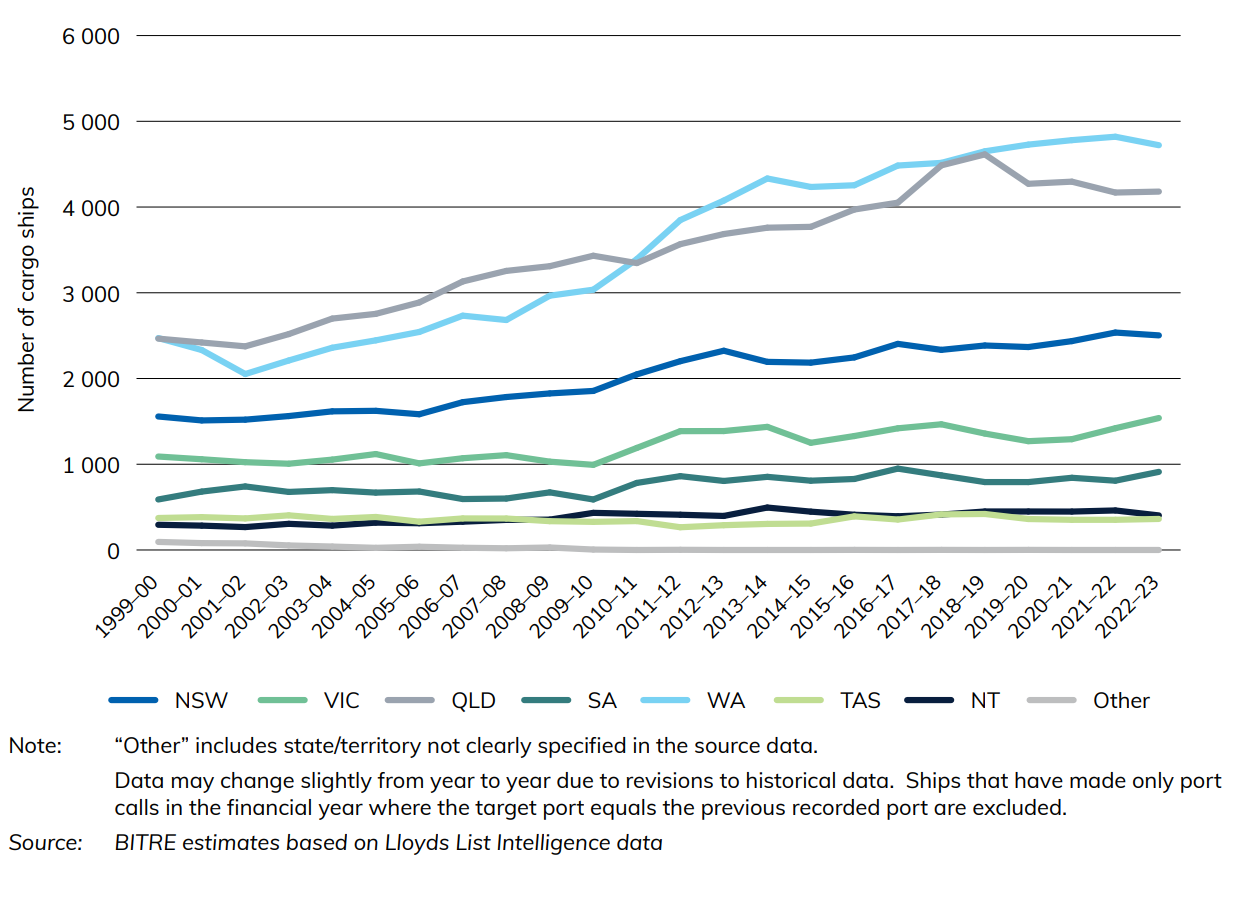

Figure 2 Number of cargo ships involved in coastal or international voyages that made port calls, by state/territory

Figure 2 provides a state breakdown of the number of cargo ships on coastal or international voyages who made port calls, from 1999-00 to 2021-22. The majority of states saw increases during this time period. Queensland and Western Australia experienced the largest numerical increases and were consistently Australia’s two most visited states by cargo ships.