Additional Maritime information can be found in the current Australian Infrastructure and Transport Statistics Yearbook 2025. Link is here.

- Time series data

- Monthly Reports and Data

- International airlines operated flights and seats

- Annual publications

Summary

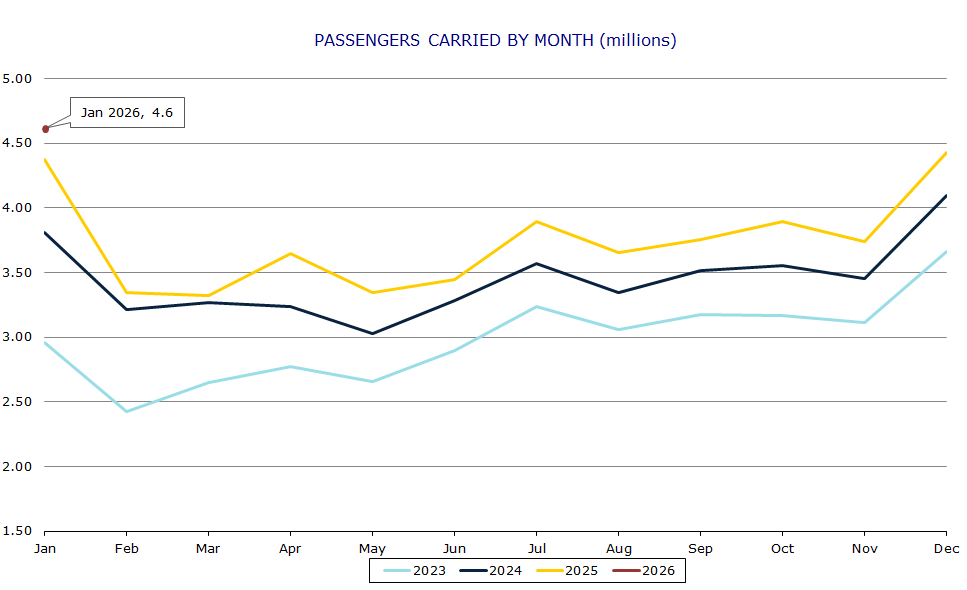

Sixty-two international airlines operated scheduled services to/from Australia during the month (includes three dedicated freight airlines but excludes airlines operating only via code share arrangements).

International scheduled passenger traffic in January 2026 was 4.620 million compared to 4.372 million in January 2025 – an increase of 5.7%. This is the third time that passenger traffic has exceeded its pre-pandemic record high of 4.154 million passengers in January 2020 (the first was January 2025 with 4.372 million and the second was December 2025 with 4.428 million).

Passenger traffic for the year ended January 2026 was 45.097 million which is a 7.6% increase over the figure for the year ended January 2025 (41.921 million).

Total seats made available on international scheduled operations to/from Australia during January 2026 were 5.610 million – an increase of 7.9% compared to January 2025. The overall seat utilisation percentage was 83.8% in January 2026. It was 85.8% in January 2025 and 81.5% in January 2024.

Summary of year-on-year activity

| Year ended January 2025 | Year ended January 2026 | Change | |

|---|---|---|---|

| Total passenger movements (million) | 41.921 | 45.097 | 7.6% |

Summary of month-on-month activity

| January 2025 | January 2026 | Change | |

|---|---|---|---|

| Passengers carried (million) | 4.372 | 4.620 | 5.7% |

| Freight (tonnes) | 93 590 | 89 151 | -4.7% |

| Mail (tonnes) | 2 021 | 1 949 | -3.6% |

| Available Seats (million) | 5.199 | 5.610 | 7.9% |

| Flights | 19 960 | 21 664 | 8.5% |

| Aircraft Movements | 20 458 | 22 082 | 7.9% |

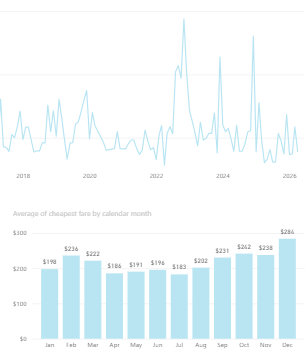

The purpose of BITRE's domestic airfare index is to monitor changes over time in the price of Australian air travel. Fares are collected monthly for the top 70 routes in the Australian domestic network.

Domestic Discount Airfares

Click the expand button at the bottom right of the dashboard to enter full screen mode.

Cheapest available return fares from January 2010

For Graphs, Summary table and Notes see further down the page. For collection methodology, see here. Collection methodology

Airfares time series from October 1992 to July 2026

Graphs

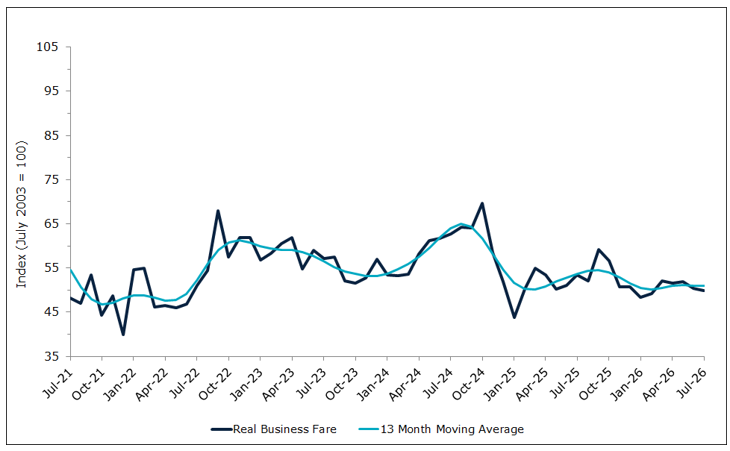

Domestic Airfares (Business)

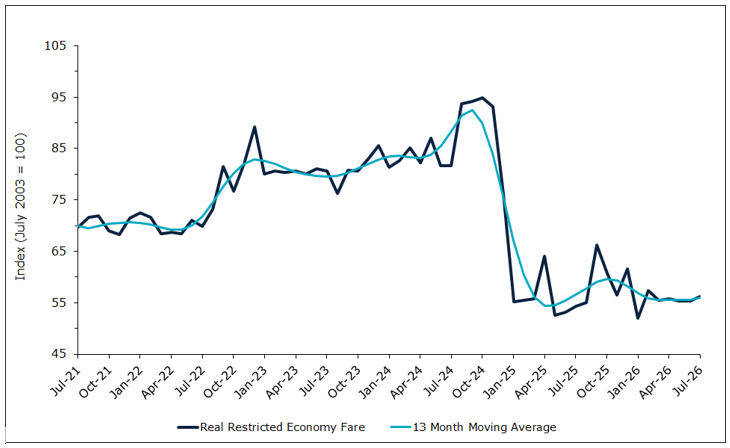

Domestic Airfares (Restricted Economy)

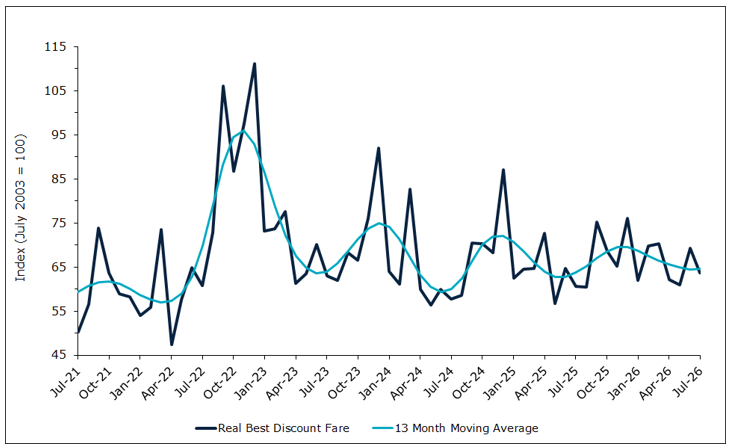

Domestic Airfares (Best Discount)

Summary table

Real Domestic Airfare Index (July 2003 = 100)

| Survey Month | Best Discount | Business | Restricted Economy |

|---|---|---|---|

| Jul 2025 | 60.6 | 53.4 | 54.4 |

| Aug 2025 | 60.5 | 52.0 | 55.0 |

| Sep 2025 | 75.2 | 59.2 | 66.2 |

| Oct 2025 | 68.9 | 57.0 | 60.9 |

| Nov 2025 | 65.5 | 50.9 | 56.7 |

| Dec 2025 | 76.3 | 51.0 | 61.8 |

| Jan 2026 | 62.3 | 48.5 | 52.3 |

| Feb 2026 | 70.0 | 49.4 | 57.6 |

| Mar 2026 | 70.6 | 52.3 | 55.7 |

| Apr 2026 | 62.3 | 51.6 | 55.8 |

| May 2026 | 61.0 | 52.1 | 55.4 |

| Jun 2026 | 69.3 | 50.4 | 55.4 |

| Jul 2026 | 63.7 | 49.8 | 56.2 |

Notes

Indexes are constructed from BITRE's monthly survey of airline internet booking sites. Fares are recorded only when they are available on the nominated day of travel (the last Thursday of the month). The series is a price index of the lowest available fare in each fare class, weighted over selected routes. It does not measure real airline yields, or average fares paid by passengers. For more information on methodology use the link at the top of this page.

Occasionally, the index may record an unusual result when the nominated day of travel falls on, or adjacent to, a public holiday:

- The travel date fell on a public holiday for April 2024, December 2024 and December 2025.

- The travel date fell the day before a public holiday for December 2020, January 2024, March 2024 and December 2025.

- The return travel date fell the day before a public holiday in March 2020 and March 2022.

- The travel date for April 2025 fell between 2 public holidays.

- The travel date for January 2025 fell after a public holiday

April 2021 to current—Best Discount index: During the period of "Half Off" air fares made available through Tourism Aviation Network Support (TANS), the BITRE Air Fares Survey has collected the cheapest available fare—using "Half Off" fares where available.

April 2021—Restricted Economy index: Virgin Australia Restricted Economy fares on some routes were noticeably lower this month. The Virgin Australia web site notes that complementary food would no longer be provided on Economy class fares as of 25 March 2021. It is not clear what part this change has played in the reductions to Virgin Australia's Restricted Economy fares.

Business class fares from April 2020: Fares collected may not include normal entitlements like meals and lounge access during the period impacted by COVID-19.

Index calculation for April 2020 to November 2020: There were significant reductions to airline services in April and May 2020 in particular due to the COVID-19 pandemic and valid fares were not available for many routes covered by the survey. The indexes for April to November 2020 are based on the available routes during those months compared to the same routes in the base period.

November 2017 change to Restricted Economy index: From November 2017, refunds of Jetstar's Restricted Economy products (Starter with Max) for cancellations are only available in the form of vouchers. Vouchers may only be redeemed for other Jetstar products and are therefore considered by BITRE to be closer to a transfer than a full refund. This change in Jetstar's product places it outside BITRE's definition of a restricted economy fare, which has resulted in a sharp increase in the restricted economy index for November 2017.

March 2015—the Full Economy index is discontinued: From the middle of February 2015, Qantas Airways ceased offering Full Economy fares for domestic travel. It is no longer possible to produce an index for this fare category. In the future, if Full Economy fares are offered on sufficient routes, the index for this fare category could be reinstated.

December 2011 and January 2012 changes to Business and Full Economy indexes: Both the Business and Full Economy indexes were substantially affected by changes to fare offered. In December 2011 the Business index fell substantially mainly due to reductions in many of these fares by Qantas. This index again dropped significantly in January 2012 as Virgin Australia introduced Business class fares on many more of their routes. With the expansion of Virgin Australia's Business class fares they removed their Premium Economy class fare completely. The removal of these fares resulted in the Full Economy index rising substantially in January 2012.

June 2011 change to Restricted Economy index: In June 2011 both Virgin Australia and Jetstar introduced simplified fare structures. The new fare types used in constructing the indexes are shown on the Methodology page. The major impact of this change was to the Restricted Economy index. The new Virgin Australia fares used for this category (Flexi) were substantially lower than the previously used Virgin fares (Flexible). In a competitive response Qantas also reduced its Flexi Saver fares on competing routes. These changes produced a sharp drop in the Restricted Economy index.

February 2008 change to Full Economy index: Prior to February 2008 the Full Economy Fare category was based solely on the Qantas Fully Flexible Fare. From February 2008 on the category was expanded to include Virgin Blue's Corporate Plus Fare, leading to a drop in the index at the point of changeover.

Consumer price index Source: Australian Bureau of Statistics, Catalogue No 6401.0. We acknowledge that the ABS has rebased CPI to September 2025 and this will be incorporated from the start of the 2026-27 financial year.

Summary of current report

This annual survey covers all civilian registered aircraft used in the Commercial Air Transport (CAT), general aviation and sport and recreation sectors of the Australian aviation industry.

The CAT sector is scheduled commercial air transport and non-scheduled commercial air transport operations. The general aviation sector is all other VH registered aircraft (other than commercial air transport). The sport and recreation sector includes aircraft registered with one of the following Civil Aviation Safety Authority regulated self-administration bodies:

- Recreational Aviation Australia (RA-Aus),

- Gliding Australia,

- Sports Aviation Federation of Australia (SAFA) or,

- the Australian Sport Rotorcraft Association (ASRA).

The major categories of flying are aerial work, own use business flying, instructional flying, personal and pleasure flying and other flying. In addition, the sport aviation segment includes operations by ultralight aircraft, gliders, hang gliders and gyrocopters. The survey results are merged with details from the civil aircraft register which gives access to additional relevant information including aircraft type, engine and fuel type, country and year of manufacture.

The base measure of this report is flying hours. All operators of Australian registered aircraft are asked to report the hours flown and landings across the various flying categories. The VH registered response to this year's reporting request was 70.2%.

Since 2020 aircraft registered with RA-Aus have been included in the annual Australian Aircraft Activity Report. The RA-Aus response to this year’s reporting request was 72.6%. Statistics for the remainder of the sport aviation segment are collected directly from the self-administrating associations.

Key Indicators

In 2024 the total hours flown in Australia by Australian owned and operated aircraft increased by 1.4% to 3.63 million hours.

CAT hours flown by VH registered aircraft increased by 1.5% to 1.93 million hours. Hours flown by scheduled commercial air transport increased by 4.7% to 1.44 million hours, while hours flown by non-scheduled commercial air transport decreased by 6.9% to 489,442 hours.

General aviation hours flown by VH registered aircraft increased by 2% to 1.4 million hours. Sport and pleasure flying hours decreased (down 10% to 221,665 hours), instructional flying (up 14.5% to 437,458 hours), own-use business flying (up 1.3% to 131,330 hours) and aerial work (down 1.4% to 542,419 hours).

Sport aviation (ultralights, gliders, hang gliders and gyrocopters) activity generally experiences large swings in activity from year to year. In 2024, sport aviation activity decreased 1.5 % to 328,574 hours.

Hours Flown in Australian Aircraft Activity (000's)—year end December

| Year | |||

|---|---|---|---|

| 2023 | 2024 | ||

| (thousands) | |||

| Commercial air transport | Scheduled | 1 371.6 | 1 436.2 |

| Non-scheduled | 526.0 | 489.4 | |

| Total commercial air transport | 1 897.6 | 1 925.6 | |

| General aviation (VH)* | Aerial work | 550.4 | 542.4 |

| Own-use business | 129.6 | 131.3 | |

| Instructional flying | 381.9 | 437.5 | |

| Sport and pleasure flying | 246.0 | 221.7 | |

| Other flying | 41.9 | 43.5 | |

| Total general aviation (VH) | 1 349.9 | 1 376.4 | |

| Sport aviation (non-VH) | 333.6 | 328.6 | |

| Total hours flown | 3 581.1 | 3 630.6 | |

*VH aircraft are registered with CASA

*non-VH aircraft are registered with self-administrating associations

Airline on-time performance statistics—monthly summary

- Airline on-time performance—monthly reports and time series data

- Airline on-time performance—annual reports (financial and calendar years)

Summary—June 2026

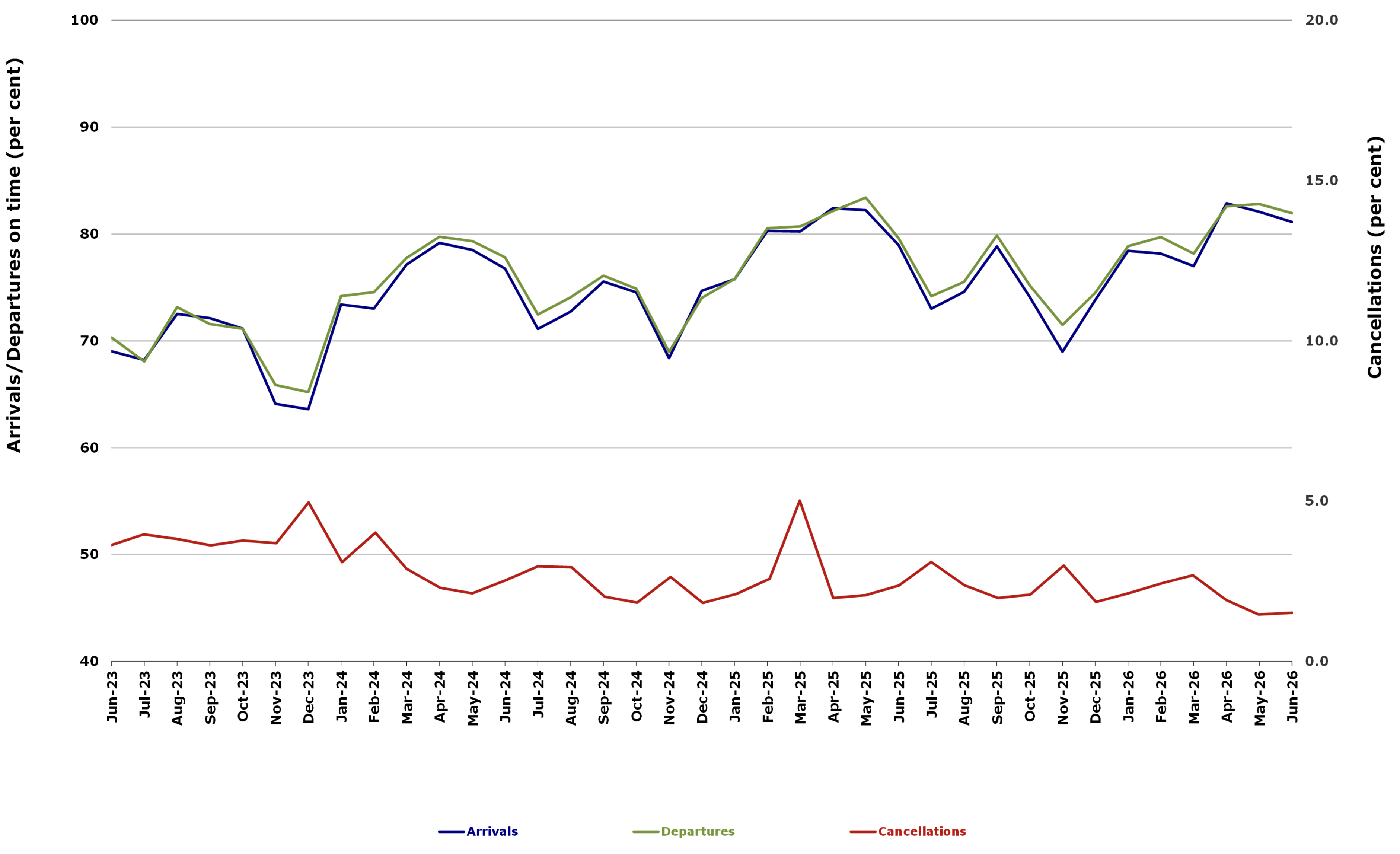

For June 2026, on-time performance over all routes operated by participating airlines (Hinterland, Jetstar, Qantas, QantasLink, Rex Airlines, Skytrans Australia (formerly SmartLynx Australia), Virgin Australia and Virgin Australia Regional Airlines) averaged 81.1% for on-time arrivals and 81.9% for on-time departures. The cancellation rate for the month was 1.5%. The equivalent figures for June 2025 were 79.0% for on-time arrivals, 79.6% for on-time departures and 2.4% for cancellations.

This month’s on-time arrivals figure was higher than the long-term average (average over the period of OTP reporting starting in November 2003) performance for all routes (80.5%) and the on-time departures figure was also higher than the long-term average (81.6%). The rate of cancellations was lower than the long-term average of 2.2%.

On-time arrivals

The Qantas network (Qantas and QantasLink combined operations) recorded 83.8% for on-time arrivals while the Virgin Australia network (Virgin Australia and Virgin Australia Regional Airlines combined operations) recorded 79.4%. Hinterland achieved the highest on-time arrivals at 93.1%, followed by Qantas at 84.6%, QantasLink at 83.4%, Virgin Australia at 79.5%, Skytrans Australia at 78.3%, Virgin Australia Regional Airlines at 77.5%, Jetstar at 76.9% and Rex Airlines at 76.2%.

On-time departures

The Qantas network recorded 84.8% for on-time departures while the Virgin Australia network recorded 80.8%. Hinterland achieved the highest level of on-time departures for June 2026 at 95.7%, followed by Qantas at 87.8%, QantasLink at 83.1%, Virgin Australia at 80.8%, Skytrans Australia at 80.6%, Virgin Australia Regional Airlines at 79.8%, Rex Airlines at 78.6% and Jetstar at 75.0%.

Cancellations

Virgin Australia Regional Airlines recorded the highest percentage of cancellations at 3.7% during the month. The second highest cancellation rate was from Skytrans Australia at 2.5%, QantasLink at 2.4%, Rex Airlines at 1.5%, Qantas at 1.3%, Virgin Australia at 1.2%, Jetstar at 0.9% and Hinterland at 0.4%.

Routes

Airlines’ on-time performance varies across the routes they serve. Individual route data by specific airline for 59 routes (118 sectors when counting both directions of flights) are shown on pages 10-21.

Of the 59 routes which met the criteria for on-time performance reporting in June 2026, the Adelaide-Canberra sector had the highest percentage of on-time arrivals (92.8%), while the Broome-Perth sector had the highest percentage of on-time departures (93.8%). The Hamilton Island-Sydney sector had the lowest percentage of on-time arrivals (62.5%) and the lowest percentage of on-time departures (54.2%).

Cancellations were highest on the Canberra-Sydney sector at 4.6%, followed by the Canberra-Adelaide sector at 4.4%, the Kalgoorlie-Perth sector at 4.2%, the Port Lincoln-Adelaide and Launceston-Melbourne sectors at 4.0%, and the Port Macquarie-Sydney, Canberra-Melbourne and Sydney-Port Macquarie sectors at 3.7%.

For the month of June 2026 35 of the 118 route sectors (from the 59 routes) had zero cancellations: Adelaide-Alice Springs, Adelaide-Gold Coast, Alice Springs-Adelaide, Ballina-Sydney, Brisbane-Cairns, Brisbane-Darwin, Brisbane-Hamilton Island, Brisbane-Launceston, Brisbane-Mount Isa, Brisbane-Newcastle, Brisbane-Proserpine, Cairns-Melbourne, Cairns-Sydney, Canberra-Gold Coast, Darwin-Brisbane, Darwin-Melbourne, Darwin-Perth, Gold Coast-Adelaide, Gold Coast-Canberra, Hamilton Island-Brisbane, Hamilton Island-Sydney, Launceston-Brisbane, Melbourne-Cairns, Melbourne-Darwin, Melbourne-Sunshine Coast, Mount Isa-Brisbane, Newcastle-Brisbane, Perth-Darwin, Perth-Newman, Proserpine-Brisbane, Sunshine Coast-Melbourne, Sydney-Ballina, Sydney-Cairns, Sydney-Hamilton Island, Melbourne-Ayers Rock.

Airports

Broome Airport recorded the highest percentage of on-time arrivals (91.4%) and the highest percentage of on-time departures (93.8%). Launceston Airport recorded the lowest percentage of on-time arrivals (72.0%) while Alice Springs Airport had the lowest percentage of on-time departures (60.0%). These figures only refer to reported routes and do not cover all flights at these airports.

Table 1: Total industry on-time performance for June 2026

| Reporting Airlines | Sectors Scheduled | Arrivals on-time % | Departures on-time % | Cancellations % |

|---|---|---|---|---|

| Hinterland | 1,632 | 93.1 | 95.7 | 0.4 |

| Jetstar | 6,944 | 76.9 | 75.0 | 0.9 |

| Qantas - all QF designated services | 18,780 | 83.8 | 84.8 | 2.0 |

| Rex Airlines | 4,081 | 76.2 | 78.6 | 1.5 |

| Skytrans Australia | 317 | 78.3 | 80.6 | 2.5 |

| Virgin Australia - all VA designated services | 11,243 | 79.4 | 80.8 | 1.2 |

| All Airlines | 42,997 | 81.1 | 81.9 | 1.5 |

| Individual operating entities | ||||

| Qantas | 6,731 | 84.6 | 87.8 | 1.3 |

| QantasLink | 12,049 | 83.4 | 83.1 | 2.4 |

| Virgin Australia | 11,109 | 79.5 | 80.8 | 1.2 |

| Virgin Australia Regional Airlines | 134 | 77.5 | 79.8 | 3.7 |

Figure 1: Total industry on-time performance by month from June 2023

Airline on-time performance—2025 calendar year

- Airline on-time performance—annual reports

- Airline on-time performance—monthly reports and time series data

Summary – 2025 Calendar Year

For the year ended December 2025, on time performance (OTP) over all routes operated by participating airlines (Hinterland, Jetstar, Qantas, QantasLink, Rex Airlines, Skytrans Australia (formerly Smartlynx Australia), Virgin Australia and Virgin Australia Regional Airlines) averaged 76.9 per cent for on time arrivals and 77.7 per cent for on time departures. The cancellation rate for the year was 2.5 per cent. The equivalent figures for 2024 were 74.6 per cent for on time arrivals, 75.4 per cent for on time departures and 2.6 per cent for cancellations. Airlines’ on time performance varies across the routes they serve. Individual route data by specific airline for 60 routes which operated for at least part of the 2025 calendar year are shown on pages 9-21.

The 2025 on time arrivals figure was lower than the long-term average (average over the period of OTP reporting starting in November 2003) performance for all routes (80.5 per cent) and the on time departures figure was also lower than the long-term average (81.6 per cent). The rate of cancellations was higher than the long-term average of 2.2 per cent.

On time arrivals

The Qantas network (Qantas and QantasLink combined operations) recorded 77.9 per cent for on time arrivals while the Virgin Australia network (Virgin Australia and Virgin Australia Regional Airlines combined operations) recorded 76.0 per cent. Hinterland achieved the highest on time arrivals at 88.4 per cent, followed by Skytrans Australia at 85.1 per cent, QantasLink at 78.3 per cent, Qantas at 77.2 per cent, Virgin Australia at 76.0 per cent, Jetstar at 75.2 per cent, Rex Airlines at 73.0 per cent and Virgin Australia Regional Airlines at 71.5 per cent.

On time departures

The Qantas network recorded 78.8 per cent for on time departures while the Virgin Australia network recorded 77.0 per cent. Hinterland achieved the highest level of on time departures for 2025 at 92.5 per cent, followed by Skytrans Australia at 86.3 per cent, Qantas at 79.7 per cent, QantasLink at 78.3 per cent, Virgin Australia at 77.2 per cent, Rex Airlines at 76.0 per cent, Jetstar at 73.6 per cent and Virgin Australia Regional Airlines at 67.6 per cent.

Cancellations

Skytrans Australia recorded the highest percentage of cancellations at 8.4 per cent during the year. The second highest cancellation rate was from QantasLink at 3.6 per cent, followed by Qantas at 2.7 per cent, Rex Airlines at 2.5 per cent, Jetstar at 2.2 per cent, Virgin Australia at 1.7 per cent, Virgin Australia Regional Airlines at 1.1 per cent and Hinterland at 0.8 per cent.

Routes

Of the 60 routes which met the criteria for OTP reporting, the Townsville-Cairns route (Jan 2025 only) had the highest percentage of on time arrivals (90.9 per cent) and the highest percentage of on time departures (90.9 per cent). For those routes reporting for the entirety of 2025, Emerald-Brisbane had the highest percentage of on time arrivals (89.8 per cent) and the highest percentage of on time departures (88.4 per cent). The Hamilton Island-Sydney route had the lowest percentage of on time arrivals (60.8 per cent) and the lowest percentage of on time departures (61.6 per cent).

Cancellations were highest on the Canberra-Sydney route at 6.2 per cent, followed by the Sydney-Canberra route at 5.6 per cent, the Port Lincoln-Adelaide and Sydney-Melbourne routes at 4.4 per cent, the Port Macquarie-Sydney and Melbourne-Sydney routes at 4.3 per cent, the Adelaide-Port Lincoln and Gladstone-Brisbane routes at 4.1 per cent, the Sydney-Port Macquarie route at 4.0 per cent and the Devonport-Melbourne route at 3.9 per cent.

Cancellations were lowest on the Melbourne-Ayers Rock at 0.0 per cent, followed by the Sydney-Hamilton Island route at 0.1 per cent, Ayers Rock-Melbourne and Sydney-Cairns routes at 0.3 per cent, and the Perth-Newman and Melbourne-Sunshine Coast routes at 0.4 per cent.

Airports

Of the airports with OTP reporting for 2025, Emerald Airport recorded the highest percentage of on time arrivals (86.2 per cent) and the highest percentage of on time departures (88.4 per cent). Port Macquarie Airport recorded the lowest percentage of on time arrivals (70.0 per cent) and Broome Airport recorded the lowest percentage of on time departures (64.8 per cent). These figures only refer to reported routes and do not cover all flights at these airports.

Table 1: Total industry on-time performance for 2025

| Reporting Airlines | Sectors Scheduled | Arrivals On Time % | Departures On Time % | Cancellations % |

|---|---|---|---|---|

| Hinterland | 18,415 | 88.4 | 92.5 | 0.8 |

| Jetstar | 96,686 | 75.2 | 73.6 | 2.2 |

| Qantas - all QF designated services | 231,962 | 77.9 | 78.8 | 3.2 |

| Rex Airlines | 52,716 | 73.0 | 76.0 | 2.5 |

| Skytrans Australia (formerly SmartLynx Australia) | 6,191 | 85.1 | 86.3 | 8.4 |

| Virgin Australia - all VA designated services | 145,379 | 76.0 | 77.0 | 1.7 |

| All Airlines | 551,349 | 76.9 | 77.7 | 2.5 |

| Individual operating entities | ||||

| Qantas | 88,886 | 77.2 | 79.7 | 2.7 |

| QantasLink | 143,076 | 78.3 | 78.3 | 3.6 |

| Virgin Australia | 143,031 | 76.0 | 77.2 | 1.7 |

| Virgin Australia Regional Airlines | 2,348 | 71.5 | 67.6 | 1.1 |

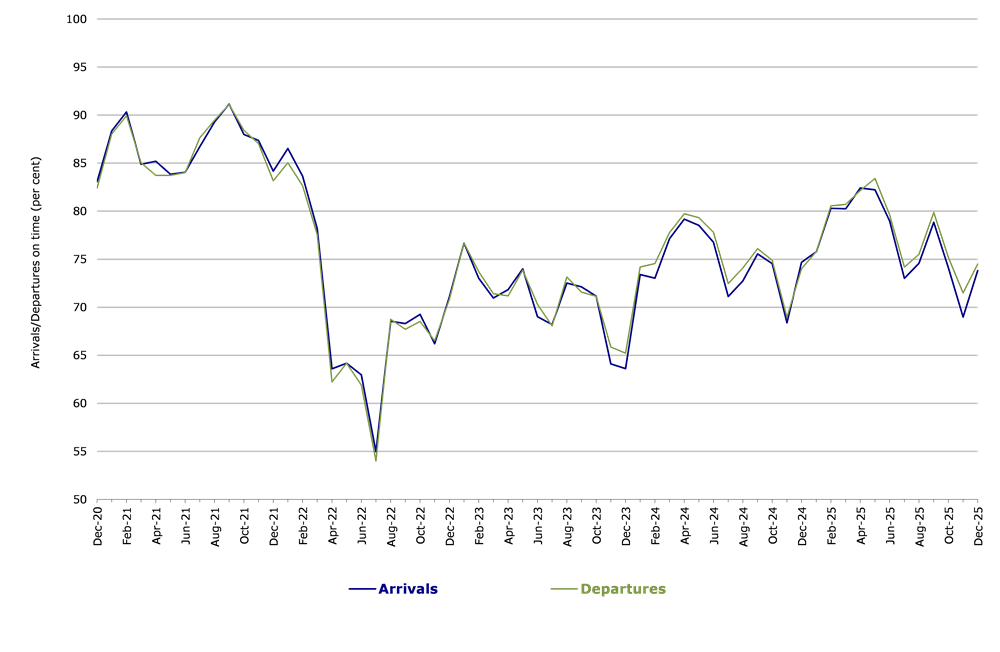

Figure 1. Total Industry Arrivals and Departures On Time by month from December 2020

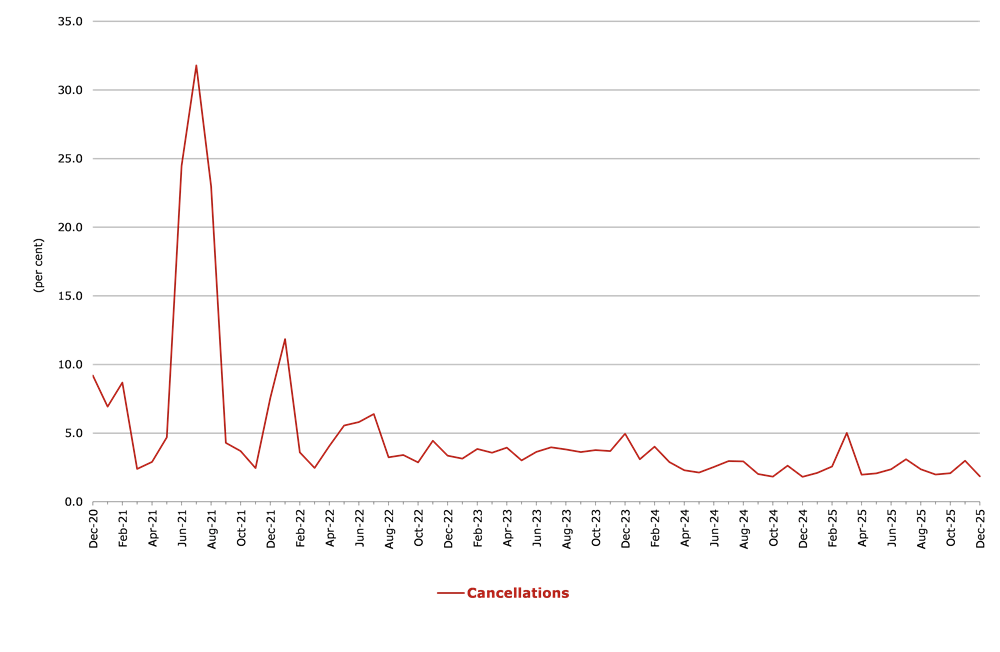

Figure 2. Total Industry Cancellations by month from December 2020

Infrastructure and the Economy - yearbook 2023

Chapter 1

Download data

This chapter provides data on the Australian economy including the value added by Australian infrastructure industries in addition to:

- employment in the transport, energy, communication and water industries

- average weekly earnings for road, rail, water and air and space industries

- price indices

- population

- 9.2 per cent of Australia’s GDP was accounted for by Australia’s major infrastructure industries in 2022-23.

- 1 million people were employed in Australia’s major infrastructure industries in August 2023.

- $1,441 is the average weekly earnings for the road transport industry in 2021.

- 84 per cent of people employed by the road transport industry identify as male.

The gross value added of major infrastructure industries as a percentage of GDP has remained relatively stable since 1974-75, generally ranging between 9-10% of GDP, with the transport postal and warehousing industry specifically ranging between 4-5% over the same timeframe. In terms of employment, although employment in the transport, postal and warehousing industry have grown in overall terms, as a percentage of total Australian employment, it has stayed at around 5% for the last 30 years.

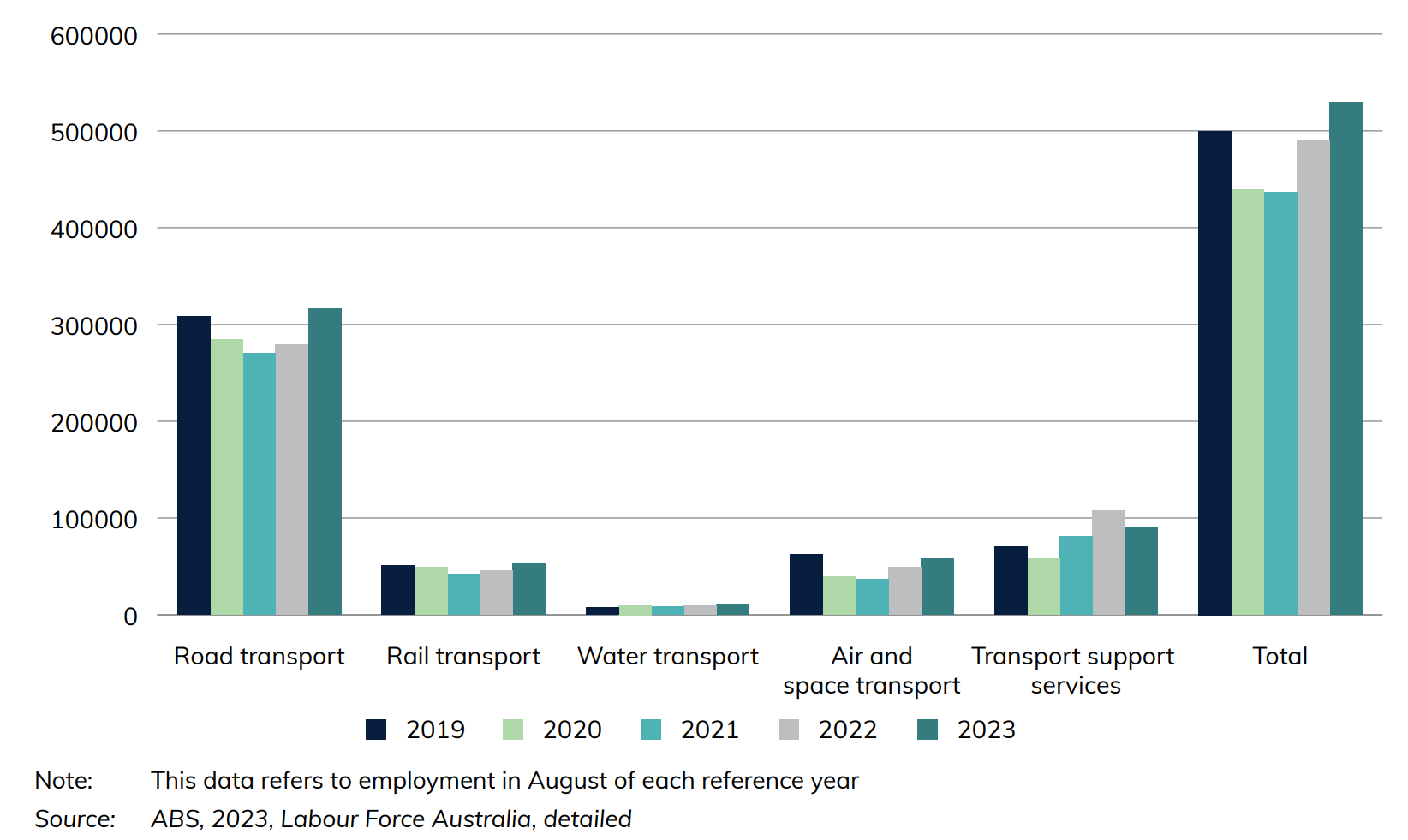

Figure 1 Australian employment numbers in selected major infrastructure industries

Figure 1 shows employment statistics for various transport industries as at August of each year. Although in 2021 COVID-19 had reduced Australian employment numbers in road, rail, and air and space transport industries, this year has shown signs of recovery, closing in on 2019 pre-pandemic levels.

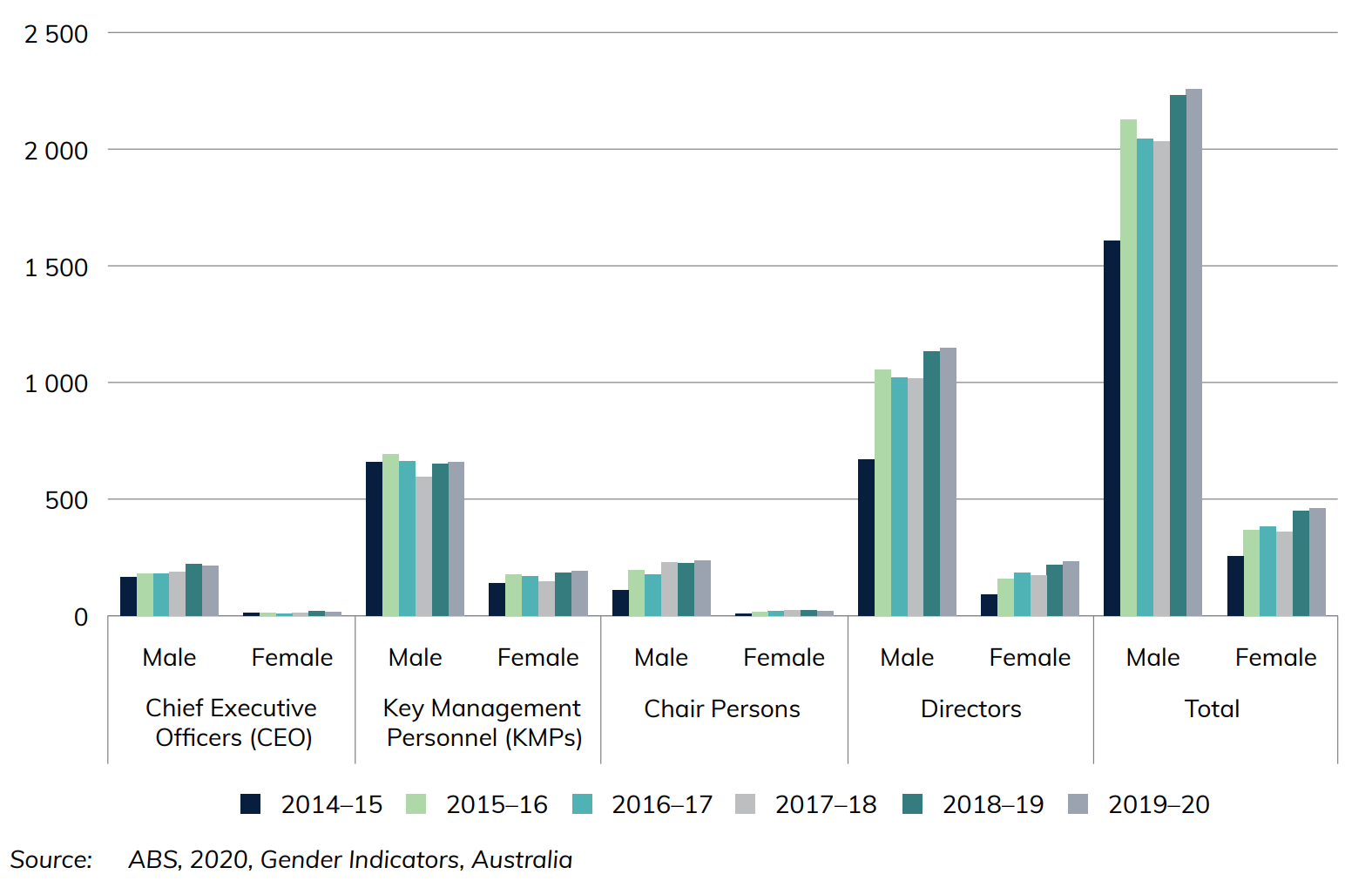

Figure 2 Leadership positions held in transport industries, by gender

Figure 2 provides an insight into gender statistics by comparing the number of leadership positions held by men and women within the transport industry. In 2019, leadership positions in the transport industry were predominantly occupied by males, with 2258 males in Chief Executive Officer, Key Management Personnel, Chair Person and Director roles compared to 460 females.

Tasmanian Freight Equalisation Scheme Monitoring Reports

The Tasmanian Freight Equalisation Scheme (TFES) provides financial assistance for cost incurred by shippers of eligible non-bulk goods moved by sea across the Bass Strait. More information about the operation of the Scheme can be found at Tasmanian Freight Equalisation Scheme | Department of Infrastructure, Transport, Regional Development, Communications and the Arts.

Under the TFES Ministerial Directions, BITRE provides a statistical report on all components of the Scheme every four years. The Monitoring Reports and other reports related to the scheme are linked below.

Monitoring Reports

- Tasmanian Freight Equalisation Scheme Monitoring Report 2024

- Consultation Draft Tasmanian Freight Equalisation Scheme Monitoring Report 2024

- Monitoring report 2020 Tasmanian Freight Equalisation Scheme

Other Reports

- Tasmanian Freight Equalisation Scheme - Review of the expanded component: Final Report (2018)

- Tasmanian Freight Equalisation Scheme: A 'Landbridge' Approach to the Estimation of Subsidy Rates (1981)

- Tasmanian Freight Equalisation Scheme: Recommended Rates of Assistance for Southbound Cargoes, Livestock and Timber at 31 January 1979

- Tasmanian Freight Equalisation Scheme: Recommended Northbound Assistance Rates at 1 January 1978

- Tasmanian Freight Equalisation Scheme: Discussion Paper September 1996

Tasmanian Freight Schemes Parameter Reviews

Australian Infrastructure and Transport Statistics Yearbook 2025: Freight chapter

Chapter 1: Freight

- Australian Infrastructure and Transport Statistics Yearbook 2025 - Download full report PDF

- Freight—Yearbook 2025 (128 KB) - Download Excel file

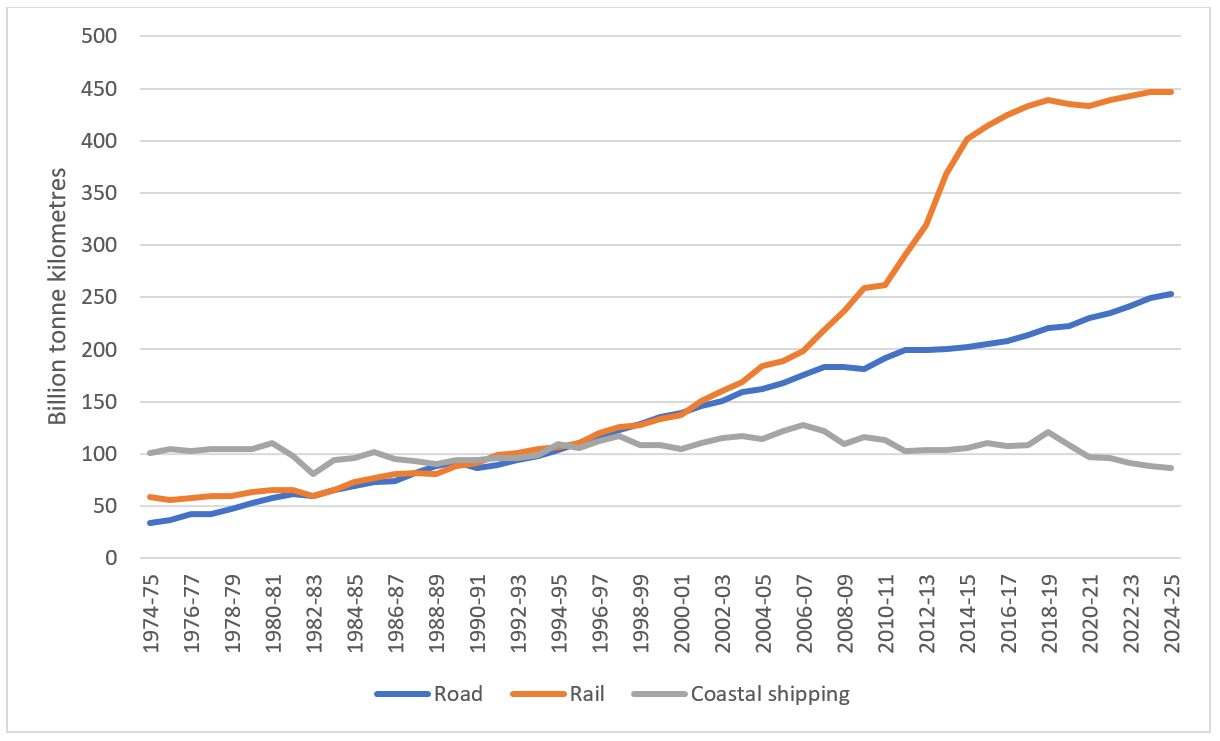

Freight transport activity (Figures 1 and 2) is measured in terms of tonne kilometres (the number of tonnes moved by a vehicle multiplied by the distance the load travelled in kilometres). The Australian domestic freight task has experienced strong growth over the last 40 years, with road and rail freight now dominating domestic freight activity.

During the COVID-19 pandemic, the total bulk and non-bulk freight task fell slightly, from 780 billion tonne kilometres in 2018–19 to 760 billion tonne kilometres in 2020–21. It has grown over the last three years and is estimated to have reached its highest point in 2024–25 at 786 billion tonne kilometres.

- Melbourne had the most metropolitan road freight estimated at 18.2 billion tonne kilometres in 2024–25.

- NSW’s estimated road freight for 2024–25 was the highest on record at 87.6 billion tonne kilometres.

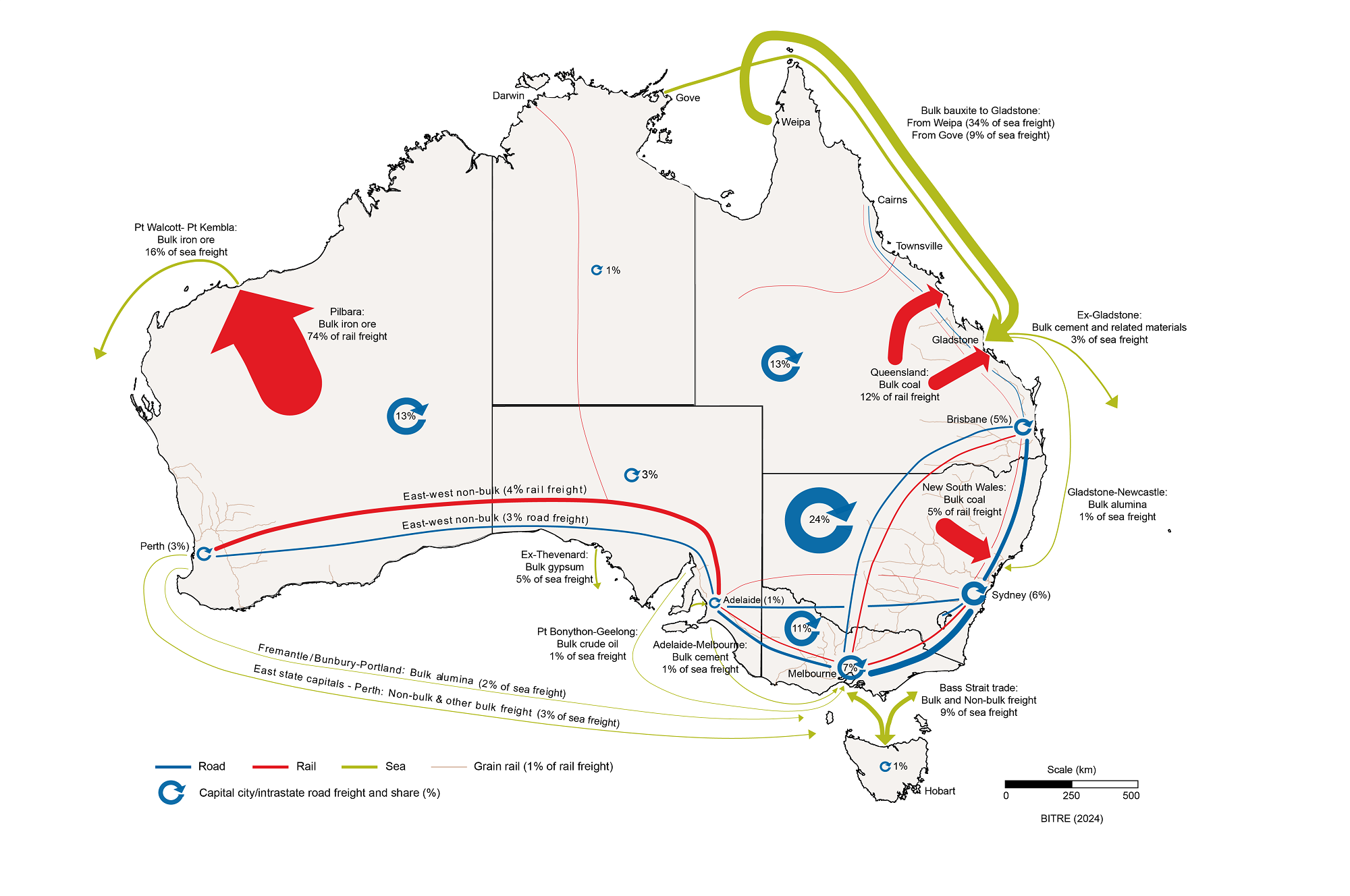

Figure 1 shows a map of Australia's major domestic freight flows by transport mode (based on 2023–24 figures). Line and arrow thickness indicate the volume of freight carried on each route, not the value of freight or performance of supply chains. The map shows that the highest volume domestic freight route is iron ore transported by rail in the Pilbara region. This next largest individual flow is coal carried by rail in Central Queensland and the Hunter Valley, followed by bauxite shipped from Weipa and Gove to Gladstone.

Figure 1 Australian Freight Flows Map

Sources:

ABARES (2024), Agricultural Commodity Statistics, March 2024, ABARES, Canberra.

ABS (2002), Freight Movements, Australia, Summary, Mar 2001 (Reissue), Catalogue no. 9220.0, ABS, Canberra.

ABS (2015), Freight Movements Australia, 12 Months ended 31 October 2014, Catalogue no. 9223.0, ABS, Canberra.

BITRE (2022), Australia interstate, intrastate and capital city road freight forecasts - 2022 update, Research Report 155, BITRE, Canberra.

BITRE (2023), Australian Infrastructure and Transport Statistics Yearbook 2023, BITRE, Canberra.

BITRE (2024), BITRE estimates, BITRE, Canberra.

BITRE, Australian Sea Freight 2023–24, Statistical Report, BITRE, Canberra ACT.

DISER (2024), Resources and Energy Quarterly, December 2023, Office of the Chief Economist, Department of Industry, Science and Resources, Canberra.

DITRDCA (2024), Coastal Trading Licensing System (unpublished data), Canberra ACT.

NFDH (2024), Freight Train Movement Data from ARTC, National Freight Data Hub, Canberra.

Qld DoR (2024), Coal production data, September 2023, Queensland Department of Resources, Brisbane.

Figure 2 illustrates Australian domestic freight activity by transport mode from 1974–75 to 2024–25. The chart indicates that rail and road account for the majority of domestic freight movement. In 2024–25, rail transported approximately 447 billion tonne kilometres of freight, while road accounted for approximately 253 billion tonne kilometres.

Figure 2 Australian domestic freight task, by mode of transport

Source: BITRE Estimates