Economic assessment of the Location Incentive on Australia's screen sector

This report assesses the current and future economic benefits of one aspect of the Australian Screen Production Incentive, the Location Incentive. The report provides an early indication on the impact of the program on the Australian screen industry and economy more broadly.

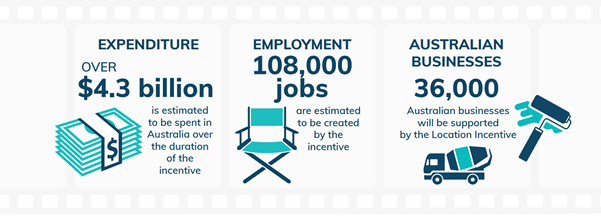

The analysis finds that the Location Incentive is projected to generate over $4.3 billion of production expenditure in the Australian economy by international film and television productions through to 2026–27.

The total program funding amount of $540 million will help Australia remain competitive in attracting international film and television productions to film here. The total number of screen productions attracted to Australia by the incentive is estimated to range from 48 to 55 by 2027.

There are also expected benefits from filming in regional areas, an expansion of Australia's screen industry, greater skills development for Australian screen sector workers, as well as regional tourism and cultural impacts.

Private sector support for the arts

The background statistical paper Private sector support for the arts in Australia highlights the essential role of philanthropy and corporate sponsorship in the sustainability of the creative sector.

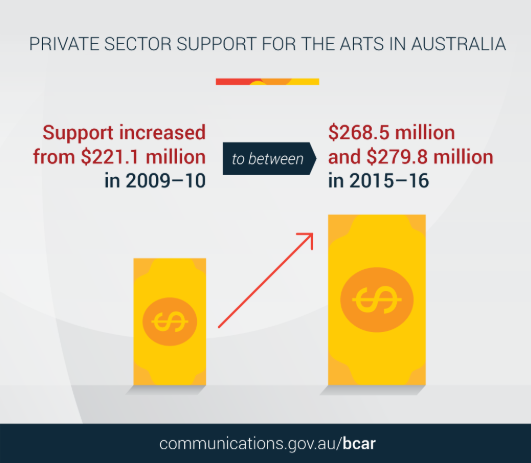

The analysis provides the first estimate of private sector support to the arts in Australia since 2009–10, which is estimated to have increased from $221.1 million in 2009–10 to between $268.5 million and $279.8 million in 2015–16.

These estimates cover a diverse range of arts organisations from small volunteer-run groups to considerably larger organisations, such as Australia’s 28 major performing arts companies.

While like-for-like comparison between countries is not possible, Australia appears to compare well internationally. Broadly, the paper estimates that Australia’s per‑capita private sector support for the arts is higher than in Canada and similar to England, though lower than in the United States.

Cultural and creative activity

Cultural and creative activity is an important part of knowledge-based economies, and it makes a valuable contribution to Australia's economic and social wellbeing.

The Bureau of Communications, Arts and Regional Research regularly publish research on Australia's cultural and creative sectors.

Key findings

Cultural and creative activity contributed $67.4 billion to Australia's economy in 2023–24. This is a 6.6% increase from 2022–23.

The cultural and creative sector contributed 2.5% of Australia's GDP in 2023–24, which is comparable to the Rental, Hiring and Real Estate Services industry.

The largest contributors were advertising and promotion, print media and publishing, film and television and architecture services.

The Cultural and creative activity in Australia 2014–15 to 2023–24 follows an updated methodology developed in 2024 to more accurately reflect the contribution of this important activity. This research is a key action of Revive, Australia's National Cultural Policy, and will assist the government with future targeted investment.

Australia’s live music sector: an occupation-based analysis

Live music is an important part of Australia’s social and cultural fabric, but there is limited information about the sector’s size and composition. This research seeks to estimate the number of workers in the live music ecosystem and their characteristics.

In the analysis, the Bureau of Communications, Arts and Regional Research (BCARR) considers all occupations required to put on a live music event. This includes primary workers, which are essential to live music (for example, musicians, technicians), supporting workers, where only a portion of their job function may involve live music (for example, ticketing, security, music teachers) and auxiliary workers, whose job indirectly supports live music (for example, hospitality staff).

Key findings

The live music sector employed 41,000 workers in 2019-20, an increase of 5,000 workers from 2015-16. This includes workers across the whole live music ecosystem, including 14,200 primary workers, 10,000 supporting workers and 16,800 auxiliary workers.

COVID-19 was highly disruptive for the live music sector. The report acknowledges the impact that the pandemic had on performances, attendance and ticket revenue.